August 29, 2025

Things I Learned This Week at Home in Dallas

There is a huge amount of news this week pertaining to our industry. Okay, it is really all about AI and the explosion of data centers. The #1 most talked about topic these days is data centers. There is no one in second place. Nothing else seems to matter. Power for data centers will need be the greenest form of energy possible. For data centers, it must also be completely reliable and “behind the meter,” so I know what my primary cost will be over the long term of my project. Wind and solar won’t work because they can’t meet the reliability standards. Nuclear could be an option, but FERC has rejected any co-location projects and selling the power behind the grid is discouraged. The last man standing? Natural Gas. Us to the rescue!

The Oil Business? An afterthought. Most of the demand for products made from oil, excluding gasoline, will continue to grow. That is mainly because so many everyday items are derived from oil and oil-based products. But don’t expect headlines. “Stranded natural gas” will be a very hot topic, since wells that can’t be economically tied into gathering facilities are ideal as a power source for data centers. Oil? Yawn. A necessary evil and that other stuff we find when we get natural gas. So much for the PR effort.

From the Horse’s Mouth. This month’s JPM E&P Shale Well Watcher report is out. “We revised our Lower 48 oil and gas production estimates. Lower 48 dry gas production has averaged 105.0 Bcf/d, up 3.4 Bcf/d. In August, production has averaged 107.3 Bcf/d, including a new all-time daily high of 108.0 Bcf/d earlier this month. August monthly production is up 9.723 Bcf/d vs. the July average of 106.5 Bcf/d, which is the highest month on record. Lower 48 oil production has averaged 13.02 MMbopd year-to-date, up 355 MBo/d compared to the 2024 average of 12.66 MMbopd through this time last year. Lower 48 oil volumes have averaged 13.18 MMbopd over August. Our lower forecast for 2025 versus our prior model is mainly driven by expected declines out of the Eagle Ford, Permian and Bakken. Updated modeling assumes a 318 Mbo/d decline in oil production in 2026, largely from the Permian (-218 MBo/d YoY). On natural gas, we are now modeling a full-year dry gas increase of 4.2 Bcf/d to 106.1 Bcf/d for 2025. For 2026, we estimate 4.3 Bcf/d of YoY growth to 110.5 Bcf/d. At the basin level, we see the bulk of 2026 growth coming from the Permian, Haynesville and Appalachia.”

Going Far North. M&A, like oil and gas production, isn’t limited to the U.S. and it is now hitting Canada hard. Cenovus has agreed to acquire MEG Energy for $5.7 billion. MEG is oil sands-focused, with its key asset being the Christina Lake project in Alberta’s Athabasca region. The project currently produces 110,000 bopd and is expected to increase by another 25,000 bopd in 2027. Strathcona made a bid for MEG earlier this year, offering about $4 billion. Through this transaction, Cenovus enhances its strategic presence in the oil sands market.

Hot Topic. The DOE has made conditional commitments to provide high-assay low-enriched uranium (HALEU) to three U.S. companies to meet near-term fuel needs for testing two advanced reactor designs. “President Trump has prioritized jumpstarting a true nuclear energy renaissance and the Department of Energy (DOE) is doing everything within its power to achieve this ambitious agenda, including increasing access to materials needed to fabricate advanced nuclear fuels,” said U.S. Secretary of Energy Chris Wright. There are currently no domestic sources of HALEU, yet many advanced reactors require the material to power the smaller designs now being developed. To address this, DOE created the HALEU allocation process, allowing nuclear developers to request HALEU from DOE sources. DOE received requests from 15 companies. In this first round, five companies were identified as meeting the prioritization criteria. Pay attention to these companies because most weren’t even on the industry radar. They include:

TRISO-X, LLC

Kairos Power, LLC

Radiant Industries, Inc.

Westinghouse Electric Company, LLC

TerraPower, LLC

Three additional companies have been selected for conditional commitments based on prioritization criteria established through the program. The companies are:

Antares Nuclear, Inc. - for use in their advanced microreactor design, which is expected to go critical by July 4, 2026, under the Department’s Reactor Pilot Program.

Standard Nuclear, Inc. - to establish TRISO fuel lines to support the Reactor Pilot Program and other TRISO-fueled reactors.

Abilene Christian University/Natura Resources LLC - for use in a new molten salt research reactor currently under construction in Texas.

More Venezuela. Last month, the Treasury Department granted approval for Chevron to resume producing and exporting Venezuelan oil. However, the Trump administration is withholding approval for several other Western oil majors seeking to operate there. The pause is focused on non-U.S. firms, leaving companies such as Spain’s Repsol, Italy’s Eni SpA and France’s Maurel & Prom in limbo.

PPHB U.S. Energy Market Highlights:

Commodity Prices: WTI crude oil is currently $64.60 per barrel (up ~1.5% week-over-week) and natural gas is $2.94 per MMBtu (up ~5.1% week-over-week).

Crude Oil Production: U.S. crude oil production is currently ~13.4 MM BOPD (up ~1.0% year-over-year).

Crude Oil Inventories: U.S. crude oil inventories decreased by ~2.4 million barrels week-over-week vs. an estimated decrease of ~1.7 million barrels.

Frac Spread Count: There are currently 165 frac spreads operating in the U.S. (a decrease of 2 spreads week-over-week).

Onshore Drilling Rig Count: There are currently 523 drilling rigs operating in the U.S. (a decrease of 1 rig week-over-week).

Snippets.

Henry Hub prices remain a staggering 70% below both the global gas benchmark and oil on an energy-equivalent basis, and it has been that way for 15 years.

AI anxiety wipes $22 Billion from Software Giants.

Welcome to Texas: Dallas police officers are now allowed to wear cowboy hats while on duty.

Natural gas accounts for 60% of Pennsylvania's electricity generation, solidifying the state as the largest electricity exporter in the country.

The Fed. Federal Reserve Bank of Dallas President Lorie Logan warned that money markets could face temporary pressures around the end of next month, though the U.S. central bank still has room to continue reducing its balance sheet. “We could see some temporary pressure around the tax date and quarter-end in September,” Logan said Monday. This is the regional Fed. They monitor our business very closely, in contrast to the national Fed, which focuses on broader measures. Bottom line? Be careful.

Sold! Nabors has long carried a difficult balance sheet, but the company has done a yeoman’s job of keeping creditors at bay, swapping tranches and paying down debt when possible. Now it has made a bigger move. Nabors, which acquired Parker Drilling in March of this year, is selling the crown jewel, the Quail Oil Tools business for $600 million. The buyer is Superior Energy, which, after emerging from bankruptcy a few years ago, is now led by Halliburton’s legacy management. Superior has been sitting on a cash hoard and borrowing capacity, and this acquisition is a big bite that fits very well with its pipe rental business. Old reputations take a long time to change, but operations can turn around much faster than perception.

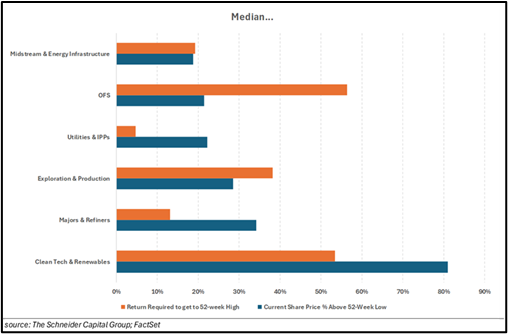

Make Up. The sector has been bashed over the last year, but how much “make up” do we need to get back to our 52-week high? The following chart from the Schneider Group shows which sectors have the most work to do. Of course, OFS “wins” on this metric.

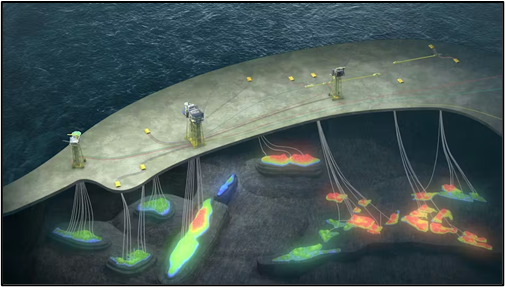

Envision: For those who don’t really know what an offshore development project looks like, this is the Norwegian Alpha project with 135 million barrels of recoverable oil.

But what does it really look like on the ocean floor?

We are in a very complex business…

Okay, I Lied. It isn’t just about energy and power. Occasionally, another topic raises its head. North Sea wind. The Dogger Bank Wind Farm, located 20-30 miles from the northeast coast of England, is being developed in three phases and will become the world’s largest offshore wind farm. Together, the projects will have an installed capacity of 3.6 GW, capable of powering up to 6 million homes annually. That certainly sounds fabulous for end users. The only problem is that the developers are expected to lose money for the next 35 years of the contract’s term. A government report says it will be unprofitable for the life of its contract. The offshore wind farm is a joint venture between SSE (40%), Equinor (40%) and Vårgrønn (20%), with Equinor operating the project. Knowing you will lose money for the next 35 years has to be a drag.

Read Between the Lines. Meta, the owner of Facebook, Instagram, WhatsApp, Messenger and more, is building its largest-ever artificial intelligence data center, a $10 billion campus called Hyperion in Richland Parish, Northeast Louisiana. The facility, set for completion by 2030, will sit on 2,250 acres of former farmland and feature a 4-million-square-foot complex. It will house infrastructure to power Meta’s next-generation large language models, including Llama. Here is where it gets interesting. “Meta pledges to power the facility with 100% clean and renewable energy.” Just not right away. The initial power will come from three natural gas-fired facilities. It will then be “matched” with renewable energy by adding at least 1,500 megawatts (MW) of new renewable energy, primarily solar and battery storage, to the grid to match its eventual electricity use. The long-term plan includes a transition towards a greater reliance on clean energy sources such as solar and potentially nuclear power. But since data centers require fully reliable power, which renewables don’t generate, Meta won’t actually run Hyperion on renewable power. Instead, it will rely on power sources to offset the natural gas power used. Of course, this adds to total emissions. It does not reduce them or even keep them neutral. Remember when United Airlines was going to plant a bunch of trees to offset the use of aviation fuel? The airline has since publicly shifted away from relying on tree-planting and carbon offsets, calling the majority of such programs a “fraud.” The company's CEO, Scott Kirby, stated that offsets are not a scalable solution to the climate crisis. I wonder what happens here.

Blowing in the Wind. President Trump stalled some wind projects off the east coast, and the reality of costs in light of agreed prices with end users has caused many projects to be scrapped. Currently, the largest commercial-scale offshore wind farm in the U.S. is the South Fork Wind Farm, which began delivering power to the New York area in late 2023 and was fully commissioned in March 2024. The Vineyard Wind Project is not yet operational. While it began partial operations and delivered its first power in January 2024, full commercial operation is not expected until late 2024 or early 2025. Remaining installation work is delayed after a July 2024 blade failure caused a temporary halt for installation work. The New Bedford staging terminal lease has been extended to June 2026 to accommodate the remaining construction. Revolution Wind is the third big player, though it is still under construction. They too are saying all the right things. Erik Milito, the president of the National Ocean Industries Association, represented the interests of the offshore oil and gas and wind industries by saying “These projects are not only about energy. They advance priorities of the Administration by restoring American manufacturing, strengthening shipbuilding, modernizing ports and building the reliable power needed to support data centers and AI innovation.” Power and energy are the objectives of the current wave of technology. This is the result:

European Snapshot. We have been writing extensively on the health of the German economy and have touched on the UK’s current situation. But we are going to look at the fiscal health of the whole of western Europe.

France is a major player in the European and global economy, but currently faces several significant economic challenges – most notably concerning its public finances and a weakening economic growth trajectory. Public debt soared to 114% of GDP last fiscal quarter. The country's deficit was 5.8% of GDP in 2024, which was the largest in the Eurozone.

Germany, while not in a technical recession, is stagnant and minimal growth is expected soon, likely in 2026. Industries have become less competitive after the stop of Russian natural gas. The hope is for a very gradual recovery, with challenges including excessive bureaucracy, high energy costs, demographic shifts and a decline in international competitiveness.

The UK's current economic outlook for 2025 is sluggish, with subdued growth prospects and elevated inflation compared to previous forecasts. While the economy is not in recession and inflation is expected to eventually fall, persistent structural issues and global uncertainty continue to temper the forecast. The Bank of England cut interest rates to 4.0% in August 2025 to stimulate the economy, but inflation remained elevated at 3.8% in July, significantly above the bank's 2% target. The labor market is softening, the cost-of-living crisis is ongoing and continues to suffer from weak productivity growth. The Public sector debt remains high, reaching 96.1% of GDP.

Italy's economic outlook is, albeit modest, marching upward by domestic demand. But a high public debt ratio, slow productivity growth and regional economic disparities do not bode well. Real GDP growth is expected to be stable, with projections of 0.7% in 2025 and 0.9% in 2026, a positive indicator for the country. The biggest issues and concerns for the country include high public debt, slow productivity growth, regional disparities, structural rigidity and bureaucracy, an aging population, trade tensions and energy dependency. That is pretty much everything.

Recommended Reading. A very good friend of mine, Scott Angelle, is the founder of U.S.A. Energy Workers. He put out an excellent piece this week:

“On this Labor Day, September 1, 2025, we pause to honor the American workforce. From teachers and truck drivers to farmers, nurses, welders and mechanics, these men and women are the lifeblood of our communities and the foundation of our economy. Among them, there is a special group whose work is often invisible yet indispensable: America’s energy workers. Every barrel of oil, every cubic foot of gas, every megawatt of electricity represents long hours, technical precision and the kind of resolve that only American workers possess. In that spirit, 2025 also marked a turning point in how our government supports energy workers. Pursuant to the authorities provided in Executive Order 14154, Unleashing American Energy, the U.S. Department of the Interior introduced long-awaited reforms to the National Environmental Policy Act (NEPA). In a landmark moment for U.S. energy policy, the One Big Beautiful Bill Act (OBBBA) was signed into law on July 4, 2025, ushering in the most significant pro-worker energy reforms in decades. The law mandates two offshore lease sales per year for the next 15 years in the Gulf of America, offers at least 80 million acres per sale and stabilizes royalty rates to promote long-term investment. Onshore, quarterly lease sales, lowered royalty rates and extended permit terms bring renewed confidence to America’s interior energy producers. The law also accelerates NEPA reviews, reinstates full intangible drilling cost deductions, supports coal and expands Alaskan energy opportunities with significant revenue sharing.”

The entire piece can be found at:

LABOR DAY 2025: Unleashing the Hands That Power America | RealClearEnergy

Sand in an Hourglass. The “evolution” of sand usage in our industry has been interesting. It was only eight years ago that we realized the sand in West Texas was perfectly acceptable for completion use, making the trains hauling North White sand from Wisconsin obsolete. West Texas has developed the mines and used trucks to move the sand to the wellsite. We now have opened over 20 sand mines feeding the Permian Basin. The basin calls for 200-250 truck loads everyday, sometimes coming from 60+ miles. We used boxes and silos to store sand on-site until needed. Then we realized that we could use wet sand, removing the expense of drying the sand at the mine using natural gas. This greatly lowered the price, especially because these mines are closer to the wellsites than the mines in Kermit and elsewhere. Atlas developed a 42-mile conveyor belt to move sand closer to the action and even automated trucks can now be seen on the road. But 200+ truckloads every 24-hours for wells drilled in the Permian is a stunningly difficult task. The load is doing damage to roads and increasing the accident rates for companies, which is a very critical concern. Now I am hearing of a technology called hydrohauling, where the sand is mixed into a slurry and is pumped in a lay-flat hose to the wellsite, providing significant savings in trucking time and reduced risk. To move the sand from the distribution center to the well pad, a patented sump blender precisely meters the sand into water to create a three-pound-per-gallon slurry. A special lay flat hose carries this slurry across the water transfer right-of-way to the well pad. There, the sand is removed and stacked in a pile that remains damp. There are constant “inventions” in the logistics of our industry. Will this be one?

Access to International Markets. This has been the goal of the OFS industry for the last 10 years and more. The U.S. is a no-growth market. Growth will be global, especially in the Middle East. This has been a well-known point for years. And now, the huge natural gas E&P company, EQT, is expanding its world. EQT signed a 20-year purchase contract for LNG to be sold to international markets. Of course, EQT already produces tons of natural gas used for domestic use, liquefaction and shipment overseas. The strategy is part of a larger plan to shift EQT's sales portfolio toward more lucrative international LNG prices, which makes perfect sense for a previously land-locked business. This will enable EQT to be a big player in U.S. gas and participate in global LNG, without the cost of constructing their own facility.

MidStream Consolidation. Harvest Midstream is paying $1 billion cash in a deal with MPLX LP for natural gas gathering and processing assets in the Uinta Basin. 700 miles of gathering pipeline with 345 mmcf/d of processing capacity. Additionally, they will get 800 miles of gathering and transportation pipes in the Green River Basin with about 500 mmcf/d of processing capacity. Harvest will supply 12,000 bbl/d of NGLs from the assets to MPLX for seven years beginning in 2028, following the expiration of a pre-existing commitment. The transaction is expected to close in Q4 of this year.

Poll: Offshore Platform Repurposing. Which repurposing strategy for aging offshore platforms offers the greatest long-term value to the offshore energy sector?

Carbon capture and storage (CCS)

Renewable energy foundations (offshore wind, wave and solar energy)

Hydrogen production and storage

Aquaculture (e.g. fish farming)

Marine research stations and artificial reefs

Meteorological/metocean research

Eco-tourism and hospitality (e.g. dive sites, floating hotels, etc.)

Rocket launch pads/offshore space ports

Misunderstood. The huge headline is Exxon talking to the Russians about oil! Obviously, a major scandal. A western oil company talking to Putin! It must be a huge conspiracy theory that is incredibly salacious. But the reality? Exxon helped develop a very large and successful natural gas/LNG facility in eastern Russia called the Sakhalin Project. It was a major project of great strategic importance for the Russian energy sector. At its peak, the Sakhalin Project was producing 670,000 barrels of oil equivalent per day. Then in 2022, the Russian government seized and nationalized Exxon’s interest, causing them to take almost $5 billion losses at the time. While the headlines look like the beginnings of some treachery, the reality is that Exxon is just trying to get its property back.

Any and all comments, arguments and rebuttals are welcome!

In addition to my association with PPHB, I serve on three private company boards. Merit Advisors is a property valuation company and I have long been a fan of optimizing how a business is run, not just the tools we make. Merit is in the business of savings companies’ money, actual cash, by doing a much more in-depth and realistic view of equipment and reserve valuations and I am very impressed with their work. I am also on the advisory board of Preng & Associates, a leading executive search boutique that specializes in all things related to Energy & Power. Nova is a gas compression company run by a very dynamic CEO with a very strong board and ownership.

I serve on the Advisory board of the Energy Workforce & Technology Council (formerly PESA), the National Ocean Industries Association (NOIA), and the Maguire Energy Institute at SMU my alma mater.

jim

214-755-3914 | james.wicklund@pphb.com

Leveraging deep industry knowledge and experience, since its formation in 2003, PPHB has advised on more than 180 transactions exceeding $11 Billion in total value. PPHB advises in mergers & acquisitions, both sell-side and buy-side, raises institutional private equity and debt and offers debt and restructuring advisory services. The firm provides clients with proven investment banking partners, committed to the industry, and committed to success.