April 24, 2026

Things I Learned This Week About Changing Temperatures

Last weekend was a blast! Two days of fly fishing on the Missouri River. The first day was a little chilly. We were hit with a couple of whiteouts, interrupted with periods of blue sky and sunshine. It is very difficult to see your fly!

Another week, and the Strait is still closed. We creep closer and closer to a global recession, yet the stock market continues to set records, which is still a bit confusing. This weekend, I am having a debate with Marshall Adkins, Mike McShane and Hance Meyers. The first topic is the correct ingredients for a real margarita, followed by the argument over which tees apply to what ages. No snow, but a great view of the Pacific Ocean.

Too much snow! Actually, I loved it. I have had a saying for years that I am sure my kids are sick of me repeating, but it has gotten me through many difficult times. If you are cold, wet, tired and miserable, but in just a couple of hours you will be warm, dry, sitting next to a fire with a wee dram of whiskey in your hand, it isn’t a hardship, but an adventure. Friday was an adventure. Saturday was just a beautiful day. But a warm beach sounds good, and I have been invited down to Mexico to have a couple of very serious discussions about the future of the oil business. The problems get easier to solve after that second margarita!

Batteries. I have given batteries a hard time for the last few years. They store power and don’t generate it on their own, and most can last for up to 2 hours, with some up to 4 hours, which never impressed me that much. Heavy, hard to make, and material prices have gone up. But things change. Batteries are now commercially competitive and failsafe assets, marking a structural shift in the sector. This wasn’t true five years ago. At that point, lithium-ion technology dominated the battery market and had for 10 years, but it was expensive, and while it worked, it wasn’t a rocket ship. From 2020 to 2024, lithium iron phosphate (LFP) technology was introduced with significantly lower cost and longer life, and it started to be used on a grid-scale basis. In the last two years, batteries have moved from a niche to core. Costs are down 90% in 15 years, and electricity demand is starting to hit the roof. Batteries offer a way to manage costs and power use, two of the most critical issues in modern business. They are becoming part of the integrated power and control systems that are taking the stage now. They are being used instead of natural gas peaker plants. Batteries are no longer just economic. They are increasingly strategic. After China manufactured more batteries than its market needed to keep its economy going, they were sold at low prices, but all are being used today. So batteries have grown up, and like compression, are having their day in the sun. I was stuck in the past, and the technology has caught me by surprise. I can still learn.

Learned. Okay, as noted above, batteries have gotten hot. I had no idea how much. CATL, a technology company in China, has built a car battery and charging system that can charge from 10% to 80% in less than four minutes and reach a full charge in 6.5 minutes. The range is 621 miles. The batteries are also cheaper since they don’t use lithium. Battery technology, after incremental improvements for years, is now undergoing its own “Moore’s Law” of development. You almost have to own a garage to own an EV, but with these charging speeds and range, two of the biggest complaints about EVs have just gone out the window. This company has a global EV battery market share of 42%, so any developments would be expected to become mainstream quickly.

Latest Survey Says. The Federal Reserve Bank of Dallas published a quick survey based on the Iran conflict. Understanding the lack of crystal balls, it provides some insight into industry expectations. Thank Garret G.

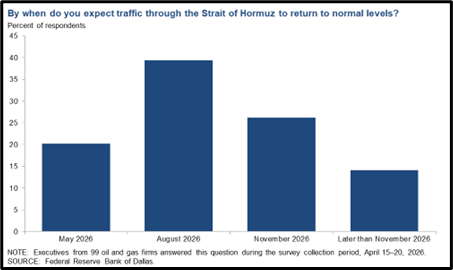

By when do you expect traffic through the Strait of Hormuz to return to normal levels? Executives expect traffic through the Strait of Hormuz to eventually normalize, although most believe it will take time. Of those surveyed, 20 percent expect traffic to return to normal by May 2026, 39 percent by August 2026, 26 percent by November 2026 and 14 percent later than that.

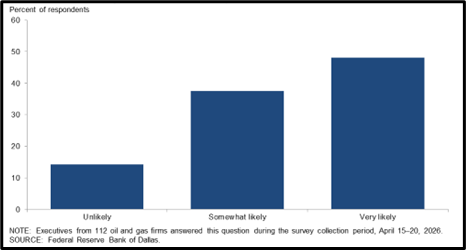

Once traffic in the Strait of Hormuz returns to normal levels, how likely is it that geopolitical events will disrupt it again within the next five years? A majority of executives say future disruptions to the Strait of Hormuz are likely. Of respondents, 48 percent say it is “very likely” that geopolitical events will disrupt traffic again within the next five years, while 38 percent view it as “somewhat likely.” Only 14 percent consider future disruptions “unlikely.”

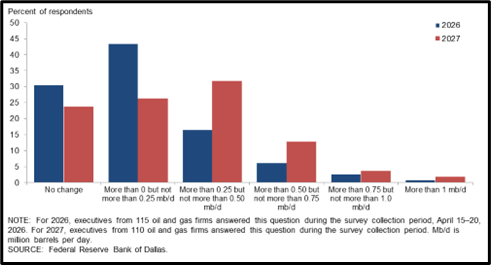

By how much do you expect U.S. oil production to increase in response to the Iran war in 2026 and 2027? Most executives expect U.S. oil production to increase in response to the conflict. The most selected response for 2026 was “more than 0 but not more than 0.25 mb/d,” chosen by 43 percent of the respondents. For 2027, the most selected response was “more than 0.25 but not more than 0.50 mb/d,” chosen by 32 percent of respondents.

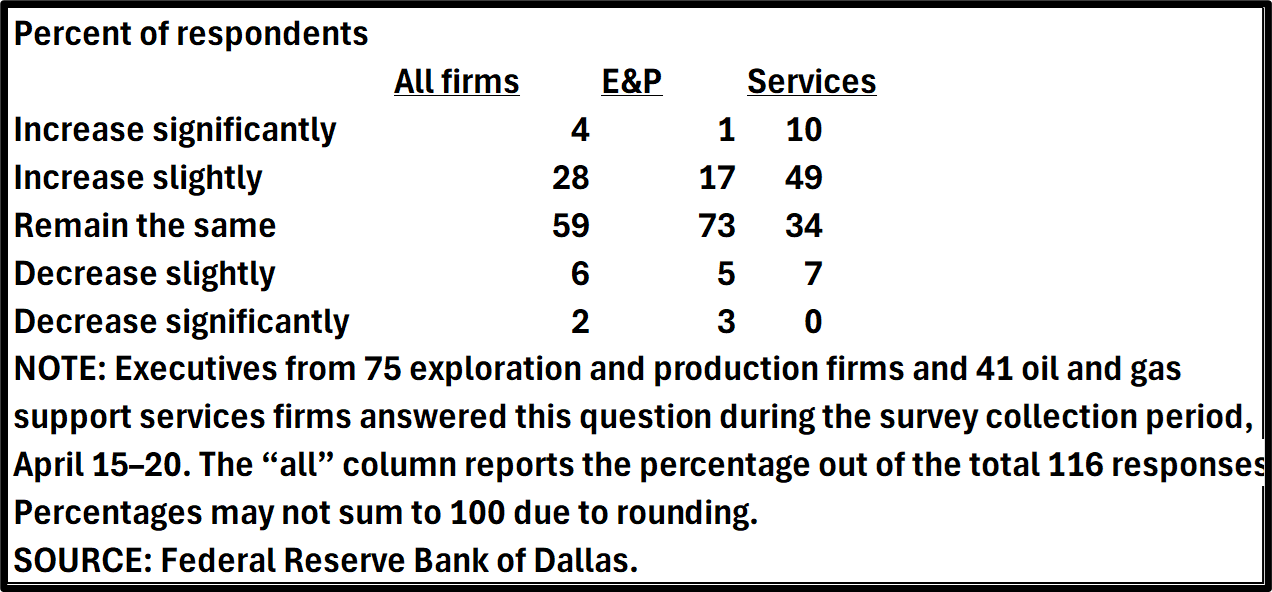

How likely are you to increase employment over the course of the next year? It shows that Oilfield Services is more likely to increase headcount than E&P, which makes sense, since, as geoscience functions can do more with less compared to field operations.

PPHB U.S. Energy Market Highlights:

Commodity Prices: WTI crude oil is currently $96.85 per barrel (up ~16.1% week-over-week) and natural gas is $3.05 per MMBtu (down ~1.6% week-over-week).

Crude Oil Production: U.S. crude oil production is currently ~13.6 MM BOPD (up ~0.9% year-over-year).

Crude Oil Inventories: U.S. crude oil inventories decreased by ~1.9 million barrels week-over-week vs. an estimated decrease of ~1.9 million barrels.

Frac Spread Count: There are currently 165 frac spreads operating in the U.S. (decrease of 6 spreads week-over-week).

Onshore Drilling Rig Count: There are currently 543 drilling rigs operating in the U.S. (decrease of 2 drilling rigs week-over-week).

Headlines.

Tanker arrives at Golden Pass LNG terminal to load first export cargo.

Observation. While the rest of the world worries about natural gas supply, top American gas companies are announcing “strategic curtailments” in Q2 because U.S. production is overwhelming demand. Javier Blas.

Broader than Known. We all know BKV Corporation, the independent that took over the Barnett Shale, the “original” shale play now over 20 years old. The company came public just last month, raising over $260 million for general corporate purposes, which would have meant more drilling 10 years ago but today can mean different things. BKV owns 75% of two gas-fired electricity generation plants in Temple, Texas, putting out 1.5 GW of power. They have a retail business with almost 60,000 customers in the ERCOT market. They are more than a natural gas producer and are trying to position themselves as a power company, the valuation dream. And they may be close, planning to finalize a power purchase agreement with an AI data center hyperscaler by early next year. That is about 7 to 8 months away, but they are narrowing and dialing in discussions. It is the continuation of a trend. Chevron and other traditional oil and gas companies are becoming power companies, not just selling their product to generate power but actually generating it themselves and staking out a position in that business. The Marcellus Shale will likely see the same. Co-location near stranded gas is key, and with Waha, the Permian natural gas hub, trading negative for much of the last 18 months, any positive price looks attractive. The trend is accelerating.

Permitting Reform. Drop what you are doing and send an email to your elected representatives and demand that permitting reform is addressed soon. Now. Over a year ago, on a trade association fly-in, we lobbied hard on both sides of the aisle for a focus on permitting reform. It makes dramatic sense regardless, even more so now in a time of energy security concerns, as it will allow us to build the infrastructure needed to support the growth of the U.S. industrial base. It should be the most bipartisan issue I can imagine, especially at a time when rapidly rising electricity demand can compound a weak grid and result in dramatic failure. “Sadly, permitting reform is often seen as a procedural issue, focusing on administrative timelines and regulatory details. This perspective is entirely incorrect. In a world of rising electricity demand, artificial intelligence expansion, industrial rivalry and grid stress, permitting reform is not procedural. It is foundational to economic stability and national security.” - Tim Tarpley

Report Back. Oilfield services companies have started reporting, with Halliburton posting a slight upside surprise, but most of the focus has been and will continue to be on the impact and outlook for activity in the Middle East. That region was expected to begin improving this year and be one of the strongest growth markets for the OFS sector. Of course, the longer the standoff lasts, the worse the economic conditions become for everyone, including the international service firms that handle the drilling, completion and production of oil and gas wells in the region. Comments from Wall Street:

“It could be that the Middle East returns to some level of activity but still carries risk of further disruption, and investors may not want exposure to that. Or maybe we get a resolution and we’re back to where we were before.” - Marc Bianchi, analyst at TD Cowen.

“In the near term, there’s definitely going to be some corrections to the numbers in the second quarter, particularly for those with Middle East exposure. There are definitely higher costs, so you’ll see some margin degradation, no doubt.” - David Anderson, analyst at Barclays.

“If the customer reduces activity, the service company suffers, regardless of the reason.” - Bianchi again.

Earnings

WFRD. Weatherford is 80% international with a strong Middle East presence so the Iran Conflict is impacting results as expected, with an estimated $30 to $50 million impact. That said, the CEO noted it was the most constructive outlook since 2023. This isn’t a cyclical issue but a structural one, with energy security now a major global priority. Lost production and storage will take years to rebuild, implying higher oil and LNG prices, increased service intensity and multi-year visibility. The company had earnings of $1.41, with free cash flow conversion of 36.5% and a line of sight to 50%+ through the cycle. Moving back to Texas, 0.5x net debt, and significant exposure to an eventual recovery.

HAL. Halliburton’s tone was different, much more cautious. The company has its greatest exposure to the U.S. shale market, which has remained in low gear for some time across both crude oil and natural gas. Activity has not responded to higher oil prices and while natural gas may be the fuel of the future, it is currently around $2.70 per Mcf, which does not support additional drilling. As a result, U.S. completion activity is weak, and pricing remains under pressure. “We are managing through a soft North American market,” and “International is strong but balanced.” However, international strength doesn’t fully offset domestic softness.

SLB. The company formerly known as Schlumberger focused on strong NOC spending, the continuation of the offshore cycle and the durability of international growth. SLB is the Iceman. No emotion, just a factual review of the situation. Sure, logistics are disrupted, cost pressures continue and conditions are constantly changing in major markets, but they remain calm, keep their head down and stay focused on execution. Not good, not bad, just what it is. Numbers get hit, the duration is unclear, but they will be there when activity picks back up. And their focus on deepwater remains core. A machine.

One Issue. The market is waiting for the usual rush of U.S. oil and gas companies starting to ramp up drilling because prices are higher than expected. That is so yesterday. Today, capital discipline is the name of the game, and everyone is playing it. The other issue is that the major oil companies who dominate the shale market today are not known for changing budgets mid-year, even if pricing improves. The “check-book” companies are almost all but history. So, while some budgets might creep up a bit as the back end of the curve rises ~$10 more than it was two months ago, don’t expect a land rush of increased activity. It is a brave new world.

If you wondered why so many past presidents have tried to acquire Greenland, the above map shows the country’s strategic significance.

Presidential Pen. President Trump has invoked the Defense Production Act, aimed at increasing power and energy in the U.S.

Presidential Determination Pursuant to Section 303 of the Defense Production Act of 1950, as Amended, on Grid Infrastructure, Equipment, and Supply Chain Capacity.

Consistent with that declaration, I find that ensuring resilient domestic petroleum production, refining, and logistics capacity is central to United States defense readiness. Petroleum fuels the nation’s armed forces, industrial base, and crucial infrastructure. Without immediate Federal action, United States defense capabilities will remain vulnerable to disruption.

Presidential Determination Pursuant to Section 303 of the Defense Production Act of 1950, as Amended, on Coal Supply Chains and Baseload Power Generation Capacity.

Consistent with that declaration, I find that ensuring reliable coal supply chains and baseload power generation capacity is essential to United States national defense. Coal mining and logistics, terminals, stockpile and power generation facilities provide indispensable resilience to our power grids that cannot be replaced. Without sufficient coal-fired baseload power, the United States will lack the stable electricity required to support defense installations, industrial expansion, and the high-energy demands of emerging technologies, such as artificial intelligence.

Presidential Determination Pursuant to Section 303 of the Defense Production Act of 1950, as Amended, on Natural Gas Transmission, Processing, Storage, and Liquefied Natural Gas Capacity.

Consistent with that declaration, I find that ensuring sufficient natural gas and liquefied natural gas (LNG) capacity is critical to sustaining United States defense operations and ensuring allied energy security. Inadequate pipelines, processing, storage or natural gas and LNG export capacity would leave the United States and its partners dangerously exposed in times of crisis.

Presidential Determination Pursuant to Section 303 of the Defense Production Act of 1950, as Amended, on Development, Manufacturing, and Deployment of Large-Scale Energy and Energy‑Related Infrastructure.

Consistent with that declaration, I find that ensuring the domestic capability for development, manufacturing, and deployment of large-scale energy and energy-related infrastructure is essential to United States national defense, yet due to financing risks, regulatory delays, and market barriers, these cannot be met in full under existing market conditions.

“I find that America’s aging and constrained electric grid infrastructure poses an increasing threat to national defense. The nation’s capacity to design, produce and deploy large-scale grid infrastructure, including transformers, high-voltage transmission components, advanced conductors, power electronics, substations and grid-supporting manufacturing equipment, is dangerously limited. These supply chains face significant risks due to foreign competition, long production lead times and overreliance on imported equipment. As a result, the United States remains vulnerable in the event of war, disaster, or economic disruption.” – President Trump.

Qualified. You graduate from college in ‘92 and go straight to law school. You graduate law school and go to work for Morgan Stanley. First job in the real world, if you can call Wall Street the real world. Seven years later, you are a vice president and the Executive Director of their M&A group. Four years later, at 36, you are appointed to the Federal Reserve Board of Directors. I would say that makes a person accomplished. This would be Kevin Warsh. I think back to all the brilliant and smart people I’ve worked with over the many years, and I think of all the up-and-coming bankers I have worked with over the years that have put in 10+ years and are starting to hit their stride. Most have, at best, made Vice President. Not a Managing Director nor an Executive Vice President, but Vice President. I think of all those young men and women as well as how many of them at that point in their careers were ready, able and qualified to be put on the Federal Reserve Board of Governors and be a key advisor during the financial crisis to Reserve Chair Ben Bernanke. Warsh was 36 when he joined the board, the youngest ever. Stanford and Harvard. Now he is at the Hoover Foundation at Stanford. Warsh is set to succeed the current Fed Chair when the seat becomes vacant. Though I find Trump’s feud with Jerome Powell ridiculous and a misguided effort, it makes the exact timing of the current Chair’s departure unknown. I don’t know the man nor his politics. I sure hope he does a good job. I am willing to give him the benefit of the doubt and wish him luck.

Seven Months In. Fermi went public just about 7 months ago and hit a valuation of $12.5 billion. Fermi is the company that former governor of Texas and former Secretary of Energy Rick Perry, his son and others founded. They are building a giant AI data center outside of Amarillo which is expected scale up to 11 gigawatts, which is huge. There are 6,000 temporary construction workers toiling away. The IPO priced at $25, ran to $32 and currently trades at $5.40. It is still a $3.4 billion market cap, but this is down 75% from when it first went public. Then, a week or so ago, the Co-Founder and CEO quit, which is never a good sign. No reasons were given by the company other than announcing, “A series of strategic and leadership initiatives under a new phase of the Company's evolution as it continues to progress along its path to becoming a mature, established entity, well positioned for long-term, sustainable growth. Following notable achievements for Project Matador across construction, buildout and regulatory milestones, these developments will position Fermi for its next chapter of innovation, operational excellence, and client-focused service.” Uh Oh. The stock dropped 30% from the news of the CEO’s departure, and the boiler plate of the above statement is not likely to defuse much. Fermi has “created an Interim Office of the CEO, which will include Mr. Jacobo Ortiz, the Company’s Chief Operating Officer, and Ms. Anna Bofa, currently an observer on the Company’s Board.” Of the four insiders who have sold Fermi shares since the IPO, only Griffin Perry, the son of former Energy Secretary Rick Perry, has sold more than Ortiz, the above mentioned Chief Operating Officer. Is the canary in the coal mine still alive?

Power Costs. I have long wondered what the latest cost comparisons are for power generation. According to EIA’s April 2026 Annual Energy Outlook for new resources entering service in 2031, estimated average levelized costs are roughly:

Natural gas combined-cycle: About $58/MWh

Natural gas combined-cycle with CCS: About $64.8/MWh

Combustion turbine / peaker: About $94.2/MWh

Advanced nuclear: About $87.8/MWh

Battery storage (Diurnal LCOS): About $152.6/MWh in the figure shown

This EIA report is important because it effectively says that short-duration batteries are not the cheapest bulk-energy source but are competing with peaker economics, not with baseload combined-cycle for pure energy cost. Short-duration batteries are the near-term winner and will dominate buildout through the rest of this decade at the very least according to the EIA, with Texas alone accounting for 12.9 GW of the 2026 additions, which is expected to add 24 GW of battery storage in 2026. Gas combined-cycle remains hard to beat on bulk-energy economics. Gas peakers are the first thermal asset most exposed to batteries. Advanced nuclear is firm and valuable, but still expensive and slow relative to batteries and gas on an LCOE basis.

California. At one point, the state had 43 refineries; This is now down to 6. Over 30% to 40% of gasoline is imported from India, South Korea and the Bahamas. The first two get their oil from the Middle East, so that will be curtailed. The state imports 61% to 63% of its crude oil.

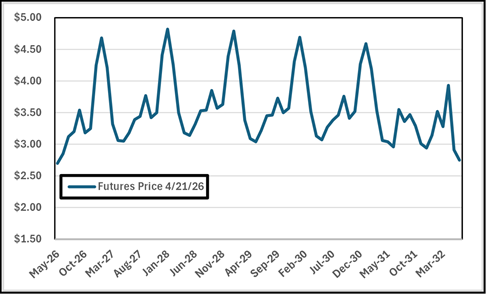

Bipolar. Remember when it was really cold in January and December before? And my birthday! Okay, around the time of my birthday, which is in early February (feel free to send late gifts!). Then winter left the building, and February and March were downright balmy. In like a lion, out like a lamb. It was the warmest ending to winter in over 15 years. And in terms of pricing in the market, the last 6 to 8 weeks of winter mattered more than the first 6 to 8 weeks because now you are managing high storage levels that are elevated as is and over-supply risk going into the summer. It has dropped natural gas to $2.80/Mcf. The futures strip below shows that while seasonal peaks look great, the overall trend appears flat to near down.

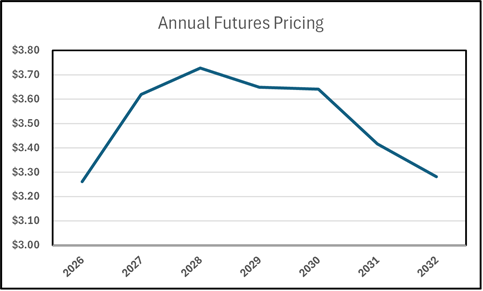

Now, to look at this from an annual average perspective, you can see that expectations are for a falling natural gas rate over the period of time that natural gas production is scheduled to growth by 25%+. Expectations of efficiency or error in judgement? The Permian could grow another 10 Bcf/d due to additional drilling, and increasing gas cuts in production. That still leaves at least us 15 Bcf/d short. The Haynesville can only do so much, and we are years away from pipes from the Marcellus. But we will somehow find and produce another 25% with a $3.50 natural gas price over the next six or so years. Personally, I am skeptical. Can you make money from existing production at a $3.50 price? Yes. Can you open up new basins and plays with a $3.50 price? No. So, increasing production by 25% in the current pricing regime is a significant challenge, especially to an industry that is now rewarding current returns over production growth. Prices go up or demand falls.

Soapbox. Iran is ruled by a religious group, part of the Muslim faith. It is a complete theocracy ruled by Shiara law. We are trying to defeat the current regime. Not for the oil, but rather the 75% of people on our side. It is what we would call a religious cult. I am by no means condemning Islam, but the ruling powers in Iran are a very fringe group. For 47 years, the country has been ruled by a supreme religious leader, and all members of the faith must do as he dictates. The country is so sophisticated. Not only does it have a great deal of oil and natural gas, but is also a country of 90 million people with a large industrial base and a very large military budget. Enough so that they had already announced enough rich uranium to build 11 nuclear bombs. This is not Venezuela. So, a sophisticated military-run country led by religious fanatics whose people believe that dying while fighting the enemy gives them eternal paradise makes having what we would call reasonable and rational discussions impossible. This is why they have no obligation to stand by any promise they make. Lying to infidels is not wrong. They are infidels. Keeping promises to infidels is the same. They are not bound by those promises and they have nothing to lose. The regime has already announced that the penalty for any protest is death, and this is after killing an estimated 30,000 people already. And now they’re doing public hangings. As Americans, we think terms like fair should always apply either in fist fights or wars. Much of the world has no understanding of the word itself. President Bush made the same mistake with Iraq, not understanding the culture of the country, the region and the religion. I thought we had gotten smarter than that. I have no recommendation to make. Armchair quarterbacking with no intelligence or information is wasted effort. It is notable that three Presidents have been swindled by this country and it is likely that more are to come. The American people need to understand the cultures around the world don’t have the same value system and worth of our society. Only 15% to 25% of Americans have ever left North America, and it isn’t all like Paris and London. This isn’t dealing with people down the street. The defeat of this regime would allow the country to enter the 21st century.

Any and all comments, arguments and rebuttals are welcome!

In addition to my association with PPHB, I serve on three private company boards. Merit Advisors is a property valuation company and I have long been a fan of optimizing how a business is run, not just the tools we make. Merit is in the business of savings companies’ money, actual cash, by doing a much more in-depth and realistic view of equipment and reserve valuations and I am very impressed with their work. I am also on the advisory board of Preng & Associates, a leading executive search boutique that specializes in all things related to Energy & Power.

I serve on the Advisory board of the Energy Workforce & Technology Council (formerly PESA), the National Ocean Industries Association (NOIA), and the Maguire Energy Institute at SMU my alma mater.

jim

214-755-3914 | james.wicklund@pphb.com

Leveraging deep industry knowledge and experience, since its formation in 2003, PPHB has advised on more than 180 transactions exceeding $11 Billion in total value. PPHB advises in mergers & acquisitions, both sell-side and buy-side, raises institutional private equity and debt and offers debt and restructuring advisory services. The firm provides clients with proven investment banking partners, committed to the industry, and committed to success.