June 5, 2026

Things I Learned This Week While Packing

More Is Less. Or Is It Less Is More? I get them confused. Either way, I am packing for another trip. This time it is Türkiye. Before you ask, as of 2022, that is the preferred spelling of the country. I will be testing how much aviation fuel is left in the country in a couple of weeks. Grueling work. There are 24 of us jumping on a Turkish gulet, which is the design of the sailboat we are on. We will bike around the islands at which we stop. It is really a 7 day floating house party. Wish me luck! As a result, no weekly next week. We are told that we won’t have WiFi for five days! Lucky me.

Another Week, Another Agreement. The latest agreement is to resume attacks, all while talking about a ceasefire. We have heard of a deal being reached every week for months now. Taking down the Iranian regime, with all the bad and evil they foment, was a very noble goal and a needed action. But religious fanatics don’t act in rational ways, especially since they fear for their lives if they hand over control. That is the “Nothing to Lose” situation for the Iranians. Now, Congress is trying to help Iran out by passing the Wars Act. As soon as the Strait opens up, the healing can start. The wound will keep bleeding and worsen if it doesn’t open. Very binary, with some nuance around the edges.

One View. Marshall Adkins is the Head of Energy Investment Banking for Raymond James, following a great career as an analyst, a hat he still wears sometimes. He held a conference call today and one message resonated. Own oil. Marshall has been an oil bull almost forever, but this time he may have a better point than in the past. You have a cushion until you don’t, and when it’s gone, you have to ration oil based on price. Marshall estimates that we have lost about 4 million barrels of demand so far due to price, but we have to lose 11 to 13.5 million barrels to balance the market. We cannot do that with sub-$100 oil. Nor does he think this will end soon while Iran is holding all the cards. And if they do open the Strait, the premium will stick around for years, since it will take three to five years to refill inventories.

The Argument. The market hasn’t paid attention to energy in 15 years, and now we have the greatest disruption to the energy markets in 70 years. Most people have no idea what is happening or what likely comes next. This will impact every part of the economy. It will take at least three months to get oil moving, though six months to two years may be needed to get back to where we were 100 days ago. Inflation, rising bond yields and a recession are in the cards. We agree. It is based on the timing of opening the Strait, but it could take some time to get back to “normal”. We have sucked inventories almost to tank bottoms, and you can’t go below that. If he is right and an agreement fully opening the Strait traffic is not done within three months, we are in print saying we will enter a global recession. That brings oil prices to $120-$160. Again, Marshall is usually bullish, and I don’t put inventories in the category of predictive performance that he does. But emptying inventories down to tank bottoms is very hard to argue with. The discussion struck me on two different points. While he is pessimistic, he is basing it on current supply and demand reality, not middle shifts at Cushing. The other is that some products may have more of a squeeze than crude oil, signaling that refiners, which have outperformed, should continue to do very well. I recommend getting the deck and listening to the replay.

My Numbers. OPEC and Middle East crude exports (UAE left the cartel) are down 10.75 million Bbl/d year over year. U.S., Russia, Venezuela and Brazil crude exports are up 3.8 million Bbl/d year over year, resulting in a net loss of -6.95 million Bbl/d. China reduced crude imports in May by 3.349 million Bbl/d year over year. South Korea is importing 0.546 million Bbl/d lower and Japan is importing 0.621 million Bbl/d less on a year over year basis. By the end of June, excess crude exports from the U.S. will go away and the SPR release of 1.3 million b/d will go to exports. So, while the U.S. will still sustain 4.6 to 4.7 million Bbl/d in exports, the net deficit will increase to ~8 million Bbl/d. Once the excess onshore crude storage is drained, each marginal barrel of demand will be bought on the physical market instead of the paper market. The true supply and demand of production will be seen. That will move oil prices higher. It is hard to know when, by how much, and how long they will stay there, but easily by August. They will stay high as we refill inventories. I will pass on guessing oil prices, but the volatility could be dramatic.

Mitigating Factors. Roughly one-quarter of the large oil tankers trapped inside the Persian Gulf have managed to slip out in a slow, stealthy trickle. 29 of the 109 bigger vessels have now crossed the chokepoint, with the cargo being snapped up by a global market where inventory buffers are shrinking. The good news is that this has added about 30 million barrels of oil supply to the market, shifting floating Gulf stock into the global commercial pool. But the bad news is that there will be fewer barrels immediately available once Hormuz reopens.

About Face. New York Governor Kathy Hochul recently signed the 2027 state budget into law and it was a surprise to many, including me. It was only 2019 when the state passed its landmark climate accords called the “Climate Leadership and Community Protection Act”. Geez. But now it has been decided that the original strict deadlines would impose “crushing costs” on New York residents. Enter the new budget. It scrapped the 2030 Mandate with the legally binding requirement to cut greenhouse gas emissions by 40% by 2030. Now it requires 60% by 2040 and is not mandatory. Kick that can. The final deadline for state agencies to finalize emissions-cutting regulations has been pushed back to 2028. The state extended its greenhouse gas accounting timeframe to 100 years. This de-emphasizes short-lived gases like methane and excludes imported fossil fuels from state totals. It looks like reason and rational thinking are taking over.

Now the Excuses Start. As with many trends that start hot, run hard, and look good, eventually the excuses start about why we have to slow down. That describes every oil and gas cycle I’ve lived through, and now it’s happening again. But this time, it is the AI trend to which I am referring. Have we ever seen a faster, harder spike up? Maybe the tech boom / Dot Com Bubble of 2000, but that’s a terrible comparison. And we get swept up in it, considering the oil and natural gas (heavy emphasis on the natural gas for these purposes) industry are some of the most critical components. The concern is that if the natural gas futures price for the next two years is only about $3.85, where are we going to get all the gas for these AI data centers? But there may be no rush. Not only are communities resisting AI data center construction, some are even banning them. The concerns about higher utility costs carry a big political stick and have started to slow down the development. Additionally, supply chain issues affect everything from turbines to transformers along with continuing permitting fights and power availability and are all being blamed for the AI data center craze cooling off.

But It Isn’t That New. Construction cancellations jumped from six projects in 2024 to twenty-five projects in 2025, according to a Baird analyst. The Financial Times recently noted that at least $156 billion of data center projects have been delayed or halted since 2025 because of local opposition, permitting challenges and infrastructure constraints. Last week, Monterey Park became the first U.S. city to enact a permanent ban on data centers after residents overwhelmingly approved a ballot measure. Other California cities have enacted moratoriums or temporary restrictions. The same report notes that at least twelve states are considering moratoriums or restrictions on new data center development. Sightline Climate estimated that 30% to 50% of projects scheduled to open in 2026 will be delayed until at least 2027, or may never be completed. The Wall Street Journal reported that more than 60% of planned 2027 capacity has not begun construction, and another 7% is already delayed. CBRE found that North American data center construction slowed in the second half of 2025 for the first time in six years, primarily due to power and electrical equipment bottlenecks.

What Are the Main Reasons Given for Delays?

Power availability (the biggest issue) - Utilities often cannot provide the required power for 100 MW to 1 GW campuses, and Interconnection queues can stretch for years.

Electrical equipment shortages - Transformers, switchgear, substations, and generators have very long lead times.

Community resistance - Concerns over water consumption, noise, land use and rising electricity costs are driving more organized opposition.

Permitting and zoning - Local governments are increasingly scrutinizing hyperscale projects.

Data centers are among the most electrical-intensive structures. Their electrical systems can represent roughly 35–40% of total project costs, making electricians, commissioning specialists and electrical contractors the critical bottlenecks. Power generation, transmission, substations, transformers, switchgear and electrical contractors may be the bigger bottlenecks.

Impressed. I met with the board and senior managers at Nabors this week following the annual meeting. I must admit, I was surprised and impressed. I have not followed the company as closely as when I followed them from a research perspective. They have paid well over $2 billion in the last few years with no real up-cycle to help them. They continue to deploy rigs in Saudi Arabia and, since they are in a joint venture with Aramco, the likelihood of their rigs working are very high. Argentina is in double figures, as is Kuwait, and more is coming. The acquisition of Parker Drilling and Quail Oil Tools after they de-levered their balance sheet by selling off equipment are a few smart purchases. Quail Oil Tools was bought for less than 2x cash flow. Overall, Nabors has made a remarkable move in the right direction over the past couple of years, boosting its international exposure and continuing to add greater technologies to its core business. I definitely think it deserves another look here.

Headlines:

“Iraq, UAE, Saudi Arabia All Set for Major Oil Output Surge in 2027”

“Venezuela Oil Exports Hit 7-Year High”

“Oil Bears Expect Regular Hormuz Tanker Traffic to Resume Soon”… No Duh.

PPHB U.S. Energy Market Highlights:

Commodity Prices: WTI crude oil is currently $93.04 per barrel (up ~6.5% week-over-week) and natural gas is $3.34 per MMBtu (up ~1.4% week-over-week).

Crude Oil Production: U.S. crude oil production is currently ~13.7 MM BOPD (up ~2.2% year-over-year).

Crude Oil Inventories: U.S. crude oil inventories decreased by ~8.0 million barrels week-over-week vs. an estimated decrease of ~2.9 million barrels.

Frac Spread Count: There are currently 192 frac spreads operating in the U.S. (increase of 3 spreads week-over-week).

Onshore Drilling Rig Count: There are currently 562 drilling rigs operating in the U.S. (increase of 4 drilling rig week-over-week).

LNG. Qatar, the owner of the world’s largest natural gas field, sustained damage that they estimate will take three years to repair. What has been produced in the Persian Gulf has been stranded for the last 100 or so days. The U.S. was already ramping up. The expectation four months ago was that the global LNG market was getting saturated, and a glut in the next couple of years might be inevitable. Then came the Iranian Conflict. Toss that glut out the window. But maybe we just kicked the can. Javier Blas is a known Middle East analyst I follow. His take:

“The Strait of Hormuz blockade triggered by the Iran war is paradoxically accelerating the global LNG market toward a supply glut. Bloomberg columnist Javier Blas analyzes that Asian buyers, seeking to break their fatal dependence on Middle Eastern energy corridors, are preparing to massively fund LNG projects in North America, Africa, and beyond, catalyzing an unprecedented third wave of capacity expansion. IEA data shows that newly approved global production capacity reached a record high of 9.8 Bcf/d last year. If all planned projects totaling 7x that amount reaches final investment decisions, supply would more than double from current levels. Meanwhile, the demand side is accelerating its shift toward solar power and coal due to price shocks. Combined with the potential return of Russian gas, these overlapping factors threaten to create a prolonged buyer's market tsunami around 2030”.

Stock Picks. Capital One gave their “Core Four: Top Picks Across Energy”. Their top four picks across the energy coverage universe over the next ~90 days are Cheniere Energy (NYSE: LNG), Murphy Oil (NYSE: MUR), Ovintiv (NYSE: OVV) and Weatherford (NASDAQ: WFRD).

2040 and Beyond! The IEA is one of the most pessimistic agencies out there when it comes to oil and natural gas. So, it was a pleasant surprise when they came out with their mid-year Energy analysis. They said the crude oil demand will continue to increase at least through 2040. Now, if you truncated your DCF at 2030 because oil demand is going away, you might want to rethink that. If you add another ten years to the DCF, the stocks are undervalued by 30% or more. It never happens all at once, but it is a trend that will continue to gain steam and attention.

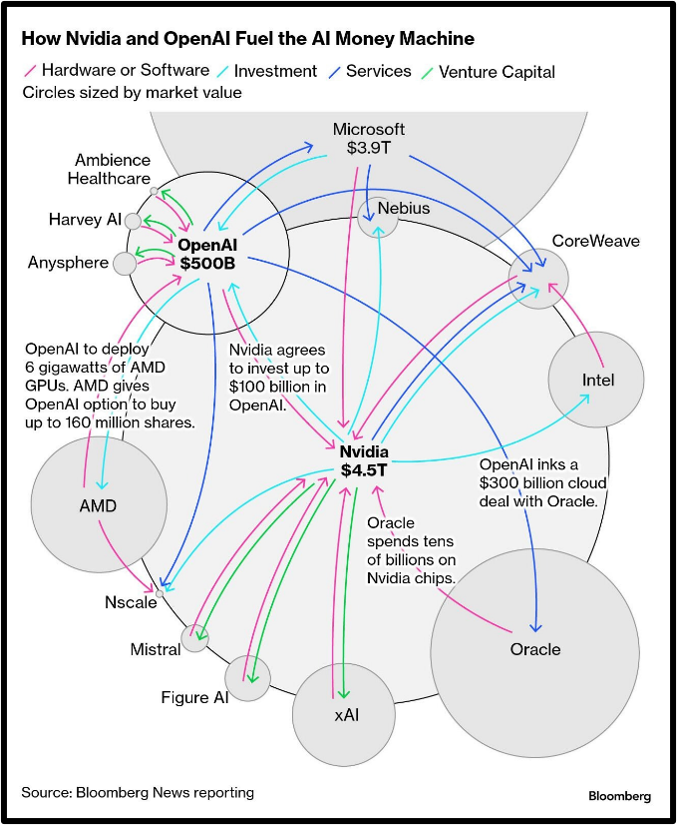

Circular Logic. Below is a chart of the AI companies’ circular spending. If one chain breaks, the entire thing breaks:

At What Cost? SpaceX revealed that Anthropic is paying $1.25 billion per month to use capacity at its Colossus data center complex in Tennessee that uses 300 megawatts of power. We are developing 25 gigawatts worth of data centers in the U.S. alone. That is $100 billion per month at those rates. It makes the $650 billion buildout sound more reasonable.

Happy Birthday. SLB (NYSE: SLB), formerly known as Schlumberger, celebrates its 100th birthday this year. The current market helps explain why the company changed its name. While it has been an oilfield services industry company for over 90% of its existence, that appears to be changing. The headline read: SLB is an "Al Factory for Energy". The stock is up 52% so far in 2026, outperforming the energy sector. Its digital strategy has always been a core competency, and it is gaining significant traction, just in a different market than before.

In Your Mind. The common perception that little progress has been made in stemming the expected dementia tsunami in the U.S. may be incorrect. The increase is expected because the large baby boom generation, born 1946 to 1964, will soon reach the ages at which the risks of dementia are the highest. The population aged 80 and older will double between 2025 and 2050, with those aged 85 and older growing 2.5 times larger, and those aged 95 and older 3.0 times larger. If age-specific dementia prevalence rates do not change, then the number of people with dementia in these age groups will grow by 2.0, 2.5 and 3.0 times, respectively, in just 25 years, justifying the tsunami metaphor.

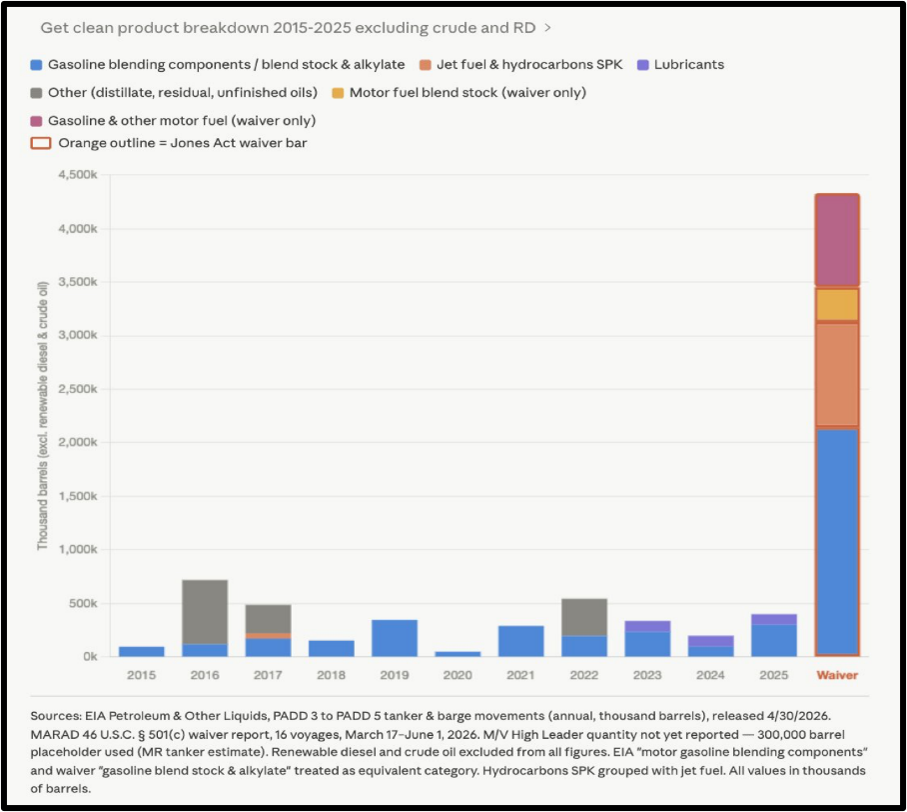

Keeping Up with the Joneses. The chart below shows the impact of suspending the Jones Act to alleviate oil and product supply issues. I will bet that it stays suspended forever. Or the legal equivalent.

Good Memory. SanDisk, at $350 billion, has seen shares rise more than 4,500% over the past 12 months. Micron was worth just over $100 billion one year ago. The memory chip company surpassed $1 trillion in market value last week, making it worth more than JPMorgan Chase. Micron shares are up nearly 1,000% over the past twelve months. Micron’s market value doubled from $500 billion to $1 trillion in less than fifty trading days, a record feat. NVIDIA, in comparison, took nearly 500 trading days to double from $500 billion to $1 trillion. Meanwhile, Seagate and Western Digital continue to benefit from data storage demand. A Barclays analyst raised his price target for Western Digital from $450 to $620. The stock is trading just below $550 and is up more than 950% in the past twelve months. It’s not just the U.S. experiencing a memory boom because of AI. In South Korea, chipmaker SK Hynix just surpassed $1 trillion in market value. Samsung Electronics achieved the feat earlier in May. Analysts expect the AI buildout to continue transforming revenue streams for companies like SanDisk and Micron.

Comparing to Tech. The above companies are just the memory companies, not the chip or other equipment manufacturers. To put it into perspective, let’s look at SanDisk. While one of the best performers, it is now worth $350 billion. And Meta is coming on the market with an $80 billion secondary offering to pay for data centers. That is the equivalent value of 100-year-old SLB! Its market capitalization is equivalent to the sum of the following companies:

Any and all comments, arguments and rebuttals are welcome!

In addition to my association with PPHB, I serve on three private company boards. Merit Advisors is a property valuation company and I have long been a fan of optimizing how a business is run, not just the tools we make. Merit is in the business of savings companies’ money, actual cash, by doing a much more in-depth and realistic view of equipment and reserve valuations and I am very impressed with their work. I am also on the advisory board of Preng & Associates, a leading executive search boutique that specializes in all things related to Energy & Power.

I serve on the Advisory board of the Energy Workforce & Technology Council (formerly PESA), the National Ocean Industries Association (NOIA), and the Maguire Energy Institute at SMU my alma mater.

jim

214-755-3914 | james.wicklund@pphb.com

Leveraging deep industry knowledge and experience, since its formation in 2003, PPHB has advised on more than 180 transactions exceeding $11 Billion in total value. PPHB advises in mergers & acquisitions, both sell-side and buy-side, raises institutional private equity and debt and offers debt and restructuring advisory services. The firm provides clients with proven investment banking partners, committed to the industry, and committed to success.