May 29, 2026

Things I Learned This Week in New Orleans

This Week Was New Orleans. The Louisiana Energy Conference started in 2000 and was founded by Al Petrie, who came from an IR background at several different oil companies. He started his practice, launched the conference and everyone had a great time. It’s in New Orleans, so the dining and wining starts off spectacularly. The conference was at The Four Seasons, so it’s hard to get more comfortable than that. Next, it was like old home week, and it wasn’t just the usual suspects at conferences. There were people I hadn’t seen in years. I think there were some 200 panelists who spoke over the course of three days, with part of the hotel dedicated to one-on-one meetings. It was like the good old days.

The Entertainment. This year, Marshall Adkins and I got to repeat our appearance from last year as two old guys sitting on stage arguing about what’s going to happen next. We’re in much more agreement now than probably ever before. Either he’s getting smarter, I’m getting dumber or we’re both getting older. It made for some interesting interactions throughout the rest of the conference.

The Intellect. Doug Terreson was featured as well. For those who don’t know Doug, he was the oil analyst at Morgan Stanley during the heyday from the late 1990s into the early 2000s, when Exxon bought Mobil, BP merged with Amoco, Total acquired Elf Acquitaine, BP acquired ARCO, Chevron merged with Texaco and Conoco merged with Phillips. I got carried away there, but damn! And we thought Exxon and Pioneer was big! Anyway, much of that happened because Doug convinced enough people that the oil companies were not being managed in a way that maximized returns. He wrote a piece called “The Pledge,” in which he asked companies to commit to capital discipline and shareholder returns pledge, helping reshape the industry in the process. It’s exceptionally rare for an analyst to have that kind of impact, but he did. He also has a book out, “I Can't Deny It” (read Chapter 9 for the reason behind the name), which is a pretty interesting read. It also explains why I could never write a book. I could never stand all those nice things being said about me.

But the conference was a success. I learned a lot, and I’ll see this week if I can apply some of the wisdom we all tried to absorb throughout the week.

Crystal Ball. One of the more interesting topics at the conference was the discussion around the next 12 months. It was a primary point of discussion on our panel, as well as for our luncheon speaker and many of the other speakers and attendees. And of course, none of us know. If you look at the Polymarket and the futures strip, there’s an 83% chance that the Strait will reopen sometime in the next two months, and the futures strip has December 2026 oil at $75. There are plenty of arguments as to why that won’t happen. I understand those arguments. I can make most of them myself. But then I look at the futures strip and start thinking with a little more nuance. I’m an optimist. I don’t think there has been any significant well damage to producing wells in the Middle East region. I understand that a great deal of work needs to be done to bring production back online, but I will take the six-month estimate for most of it rather than the 12-to-18-month timeframe I hear bandied about. There’s also the floating inventory inside the Arabian Gulf, which some people already classify as inventory, even though much of it was loaded for delivery. We will talk about that later. If the Strait opens fairly soon, the conventional wisdom is that it will take some time for traffic to return to normal. The problem is that traffic has to be well above normal to clear all of the excess inventory and congestion on either side of the Strait. Once it’s open, you would think it would stay open. Then again, it was declared open a couple of weeks ago for a few seconds. The longer this lasts, the more damage is done to the global economy. Southeast Asia gets hurt the worst, while U.S. consumers get hurt the least. There’s been surprisingly little demand destruction in U.S. gasoline consumption so far, which is somewhat surprising given all the media attention gasoline prices get.

The Vibe. The mood was interesting. U.S. onshore activity is holding up better than expected. Nobody is really adjusting activity or budget levels higher yet, other than a very, very few outliers. Nor are they slowing down as much as they, and everyone else, had expected. So that’s good for U.S. onshore. U.S. onshore pricing across many service lines is starting to move up after years of consolidation and equipment deterioration. It has taken a decade to get equipment supply and demand back into balance, but it’s starting to happen, and pricing is beginning to improve. Rig demand is creeping up at a glacial pace, but operators are making good money, and that always has some trickle-down effect on service companies. While current and recent oil prices have been amazing, the futures market expects a return to something more normal, or at least lower. The WTI crude strip for the next 12 months averages $81.38 per barrel, with the 24-month strip at $78.50 per barrel. It will be interesting to see at what prices deals get done. Natural gas activity hasn’t budged much, but neither has the price. The current price is around $3. For natural gas, the 12-month Henry Hub strip is $3.31 per MMBtu, with the 24-month strip at $3.42 per MMBtu. That is not high enough to meaningfully increase drilling activity, yet the LNG and data center markets need another 5 Bcf/d over the next five years. Something has to give.

A Very Interesting Point. There are ships that have been trapped in the Persian Gulf for almost three months, loaded with oil. The volume is estimated at about 200 million barrels. When the Strait is reopened, that oil will start moving out. Some people I spoke with said those volumes were already included in their models, usually as storage inventory. But most of this oil was not loaded onto ships with the intention of being stored. It was loaded to be delivered to contracted buyers. That means it effectively becomes inventory liquidation, moving to market as fast as it can. The trip from the Persian Gulf to the U.S. Gulf Coast takes about 28 days. One point that was raised is that oil prices may very well drop when the Strait is reopened, and perhaps fall a bit more as oil begins to flow again. But a month later, when as much as 120 to 150 million barrels have been “liquidated out of inventory,” oil prices could see another leg down. One analyst recommended buying half of a position when the Strait actually reopens and the other half a month later, as the surge of stored oil reaches the market. It won’t have a long-term effect. Inventories in general are already low and need to be rebuilt, so demand for oil should stay strong. But like a tennis ball moving through a snake, it may take some time for the overshoot and undershoot to work their way through the system before jumping back in with both feet. There are also 6.5 million barrels of refined products waiting to be freed.

Moore’s Law. Drilling efficiencies have been remarkable, and so have completions. There are physical limits to how fast you can move pipe and overcome other mechanical issues, but completions still have significant room for improvement. We can get much smarter. One panel of E&P executives were talking about how technology and innovation have changed the business, citing examples such as reducing drilling times from 30 days to 15 days. The question was raised whether most of the major efficiencies and technological advancements have already been made and whether the industry is now simply pursuing incremental improvements. All of the participants were smart enough to say no. They acknowledged that drilling has made amazing advances and will continue to make more, but they emphasized that completions technology and efficiency gains are still moving at a rapid pace. One example cited was recovery rates. Unconventional oil recoveries are typically in the 6% to 8% range, while conventional recoveries are closer to 47% to 50%. As a result, many believe that large gains are still to be made. Technology development has not stopped. In fact, it is being applied most aggressively in areas focused on optimizing production while maximizing returns.

Ahead of His Time? We have moved into a new period of time. This is when you realize your old profession has moved in for some other. And you might be in that “some other” category. What makes me sound so morbid and depressed, yet impressed at the same time? A piece of research from a great analyst (worked with me!) caught my attention: “U.S. military strikes in Iran sent Polymarket odds to…”. No reference to oil prices or gasoline prices, nor rig counts or day rates. No EBITDA or ROIC valuations. Polymarket odds. In case you didn’t know, Polymarket is a decentralized prediction market that allows users to trade financial shares based on the real-world outcomes of future events. Rather than playing against a traditional bookmaker, users engage in peer-to-peer trading where they buy “Yes” or “No” contracts on topics spanning across politics, culture, sports, and science. It is a private company with an estimated value of $15 billion. The valuation tells you how big a market is. No bookie means heads-up betting, and you can bet on any number of things. The best odds for oil prices shows an 83% chance that oil prices will be below $90 by the end of June. Don’t think so? Place a bet. Besides, now betting has been elevated to the first bullet point of an equity analyst’s report.

Polymarket. “The smartest way to follow world events and trade what happens next.”

An Example of Volatility. “U.S. military strikes in Iran sent Polymarket odds for Strait of Hormuz traffic returning to normal by the end of June to 44% this morning, down from 59% on Saturday, May 23rd, but up from the trough of 26% on Sunday, May 10th. Odds of traffic returning to normal are 62% by the end of July and 87% by the end of December.”

Back Story. Several years ago, I wrote about the expansion of the Panama Canal. Many economists were saying that it would be one of the best investments and most impactful actions seen in a decades. The expansion was 10 years ago. There are a couple of things I learned. The expansion of the canal allowed LNG to transit to Asia, allowing the U.S. Gulf Coast LNG industry to flourish. Now about 25% of LNG from the U.S. goes to Asia and most of that is through the canal. I did not know that it was water dependent. Now, you’re asking yourself “what does that mean?” I did not know that the Panama Canal depends on rainfall and a freshwater lake. If it doesn’t rain, some ships, especially LNG tankers, can’t transit and have to steer around Africa, adding significant time and money and emissions, which still matter. And at times, the Canal has been closed to LNG carriers for a month. All of this is part of the impact of the expansion of the Canal, whose revenues have doubled, and its Chinese-owned ports of Balboa and Cristobal have become the poster children of U.S.-Chinese relations. Little things that we usually take for granted and something I learned this week.

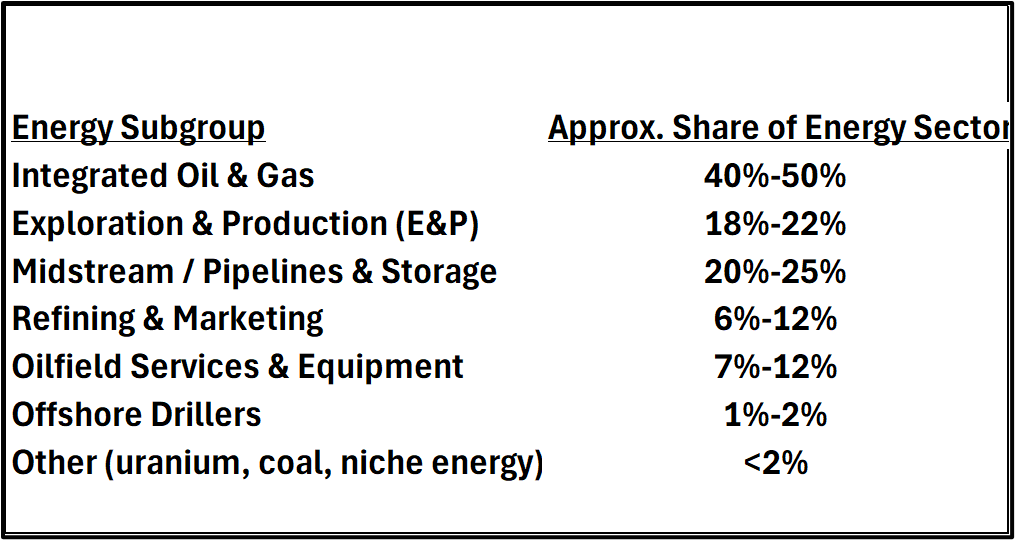

The Energy Sector. We all talk about how the energy sector in the S&P 500 is relatively small today, roughly 3–5% of the index, depending on oil prices and market moves. But I got curious as to the make-up and relative performance of the components.

So, the sector is dominated by integrated major oil companies, midstream infrastructure companies and shale E&P companies. The majors act more like utilities, with high dividends, big stock buybacks, and have chemicals and LNG as well. E&P just finds and produces, so are more sensitive to commodity prices while midstream is more of a toll road with increasing volumes. Oilfield services has the highest volatility and are hyper-cyclical; refiners are more about the spread of pricing more than the price itself.

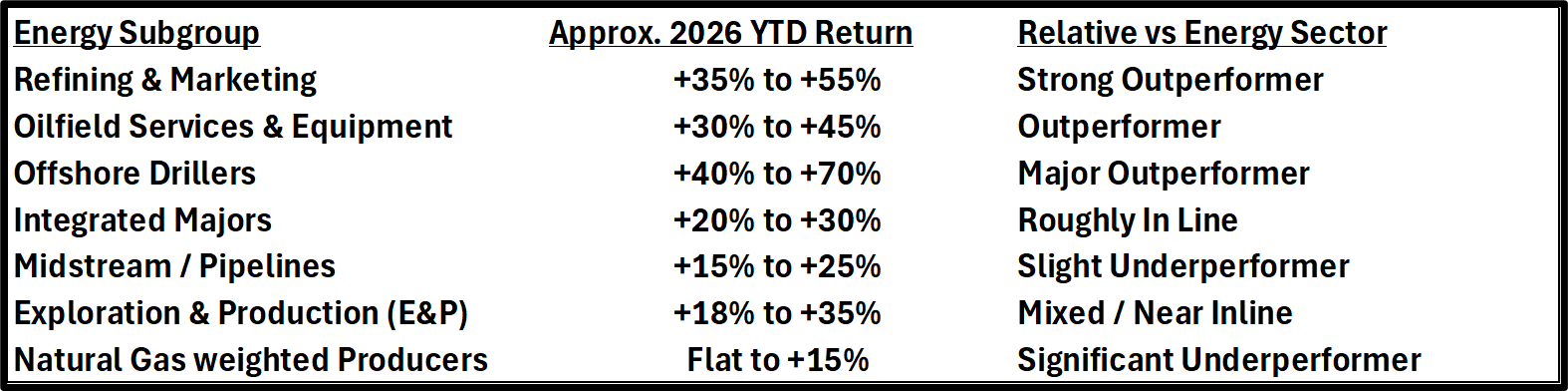

Year to date in 2026, the energy sector has dramatically outperformed the broader S&P 500, but the gains have not been evenly distributed across the energy subgroups. The biggest winners have generally been the most cyclical and operationally leveraged areas of the market. They feed on volatility.

PPHB U.S. Energy Market Highlights:

Commodity Prices: WTI crude oil is currently $88.90 per barrel (down ~7.8% week-over-week) and natural gas is $3.29 per MMBtu (up ~8.4% week-over-week).

Crude Oil Production: U.S. crude oil production is currently ~13.7 MM BOPD (up ~2.3% year-over-year).

Crude Oil Inventories: U.S. crude oil inventories decreased by ~7.9 million barrels week-over-week vs. an estimated decrease of ~7.9 million barrels.

Frac Spread Count: There are currently 184 frac spreads operating in the U.S. (increase of 5 spreads week-over-week).

Onshore Drilling Rig Count: There are currently 558 drilling rigs operating in the U.S. (increase of 7 drilling rigs week-over-week).

The strongest performers inside energy have generally been:

Offshore drillers like Transocean and deepwater service companies

Refiners such as Marathon Petroleum and Valero Energy

Oilfield service leaders including SLB and Halliburton

Meanwhile, the relative under-performers were:

Midstream pipeline operators

Natural gas-heavy producers

Large integrated majors

Tech IPO. The energy business can be right up there with the highest of tech companies sometimes. Witness the recent IPO of Fervo, up over 40% from its IPO price, valuing the company at over $12 billion despite no revenues. Wow, right? But it isn’t a tech company. It is a start-up geothermal company. Geothermal is cycling water / steam through very hot spots in the subsurface to generate electricity and power. The company has signed over $7 billion in power supply projects, representing 658 megawatts of power. The first kicker? If they don’t meet the first delivery schedule, they pay their customer. The second kicker is that they have not generated any power yet. Over $12 billion. Geothermal is one of the cleanest power generating sources, but it is geographically contained. Utah is the site of the company’s first project, and the company estimates it will eventually develop 42 gigawatts across Utah, Idaho and Nevada. Its first project is scheduled to start in Utah soon and kick off the revenue generation part of the business. Clean energy isn’t dead, but investors believe it will be a really big thing. We shall see.

How Much? There was a story this week about how E&P M&A activity was testing the waters to see if there are any buyers in the current commodity price environment. Our last estimate on deals pending is probably around $5 billion. But whether the Straits are open or closed, oil prices do still matter. It shouldn’t so much. The current future strip for oil has WTI at $75 in December. Nobody's going to want to sell on that basis, even though it is realistic and buyers think it's a good idea. It’s just the evaluation of the intervening months that skews the economics. It also made an interesting point, that instead of the major oil companies sucking up the big E&Ps, it's now the big E&Ps and the small ones consolidating themselves. One can argue they’re doing it just to make themselves more attractive to a major buyer, but whatever the reason, it seems poised to happen. According to Polymarket, there’s an 83% chance that the Straight is opened within the next six months, putting oil at a $75 December price. But, of course no one knows when that’s going to happen exactly. It hinges on whether we have another air strike or not. President Trump is in between a rock and a hard place. Netanyahu must have convinced him that Iran would capitulate fairly quickly. It’s assault. We’ve said before, that without the participation of the people, nothing will change, and the people have no guns and are threatened with hanging if they protest. It’s a game of economic chicken, and the Iranians know the importance of the midterm elections, so they are most likely to do what they always do which is prevaricate and delay. Whether all of this gets resolved in the U.S. M&A market will dictate whether oil and natural gas companies pick up again. No one knows. But, once the price forward gets settled, we would expect at least a small tsunami of deals to get done. They will have a great deal of time to have percolated.

Lagnappe. The Thursday morning presentations at the LEC featured companies that define innovation; Some come around almost by accident. A very interesting e-learning company that takes training and recertification in the oil business to amazing levels did so through a petroleum engineer being assigned a training job at a little Louisiana oilfield services firm. A film and movie support business who developed mobile distributed power capability that stretches from FEMA support, powering movie lots, and now, data centers. Select is an established water company, recycling more water in the Permian than anyone else. It found it can extract lithium and iodine at a very economic value at significant volumes.

Hollywood Truck Technologies

ICAN Technologies

LibertyStream Infrastructure Partners

Select Water Solutions

Major Moves:

Chevron shareholders reject proposal for independent board chair

BP’s board fires Chairman

Exxon shareholders approve redomicile to Texas from New Jersey

Any and all comments, arguments and rebuttals are welcome!

In addition to my association with PPHB, I serve on three private company boards. Merit Advisors is a property valuation company and I have long been a fan of optimizing how a business is run, not just the tools we make. Merit is in the business of savings companies’ money, actual cash, by doing a much more in-depth and realistic view of equipment and reserve valuations and I am very impressed with their work. I am also on the advisory board of Preng & Associates, a leading executive search boutique that specializes in all things related to Energy & Power.

I serve on the Advisory board of the Energy Workforce & Technology Council (formerly PESA), the National Ocean Industries Association (NOIA), and the Maguire Energy Institute at SMU my alma mater.

jim

214-755-3914 | james.wicklund@pphb.com

Leveraging deep industry knowledge and experience, since its formation in 2003, PPHB has advised on more than 180 transactions exceeding $11 Billion in total value. PPHB advises in mergers & acquisitions, both sell-side and buy-side, raises institutional private equity and debt and offers debt and restructuring advisory services. The firm provides clients with proven investment banking partners, committed to the industry, and committed to success.