April 3, 2026

Things I Learned This Week in Meeting After Meeting

Bouncing Around. The first meeting was a pleasure. A conservation organization I belong to had its annual Investiture last weekend in Sea Island, Georgia. The International Order of St. Hubertus. More on that later. Then came the 80th Annual TIPRO meeting, the Texas Independent Producers and Royalty Owners. These guys are the heart and soul of our industry. They have granular views on prospects and valuations that the big public companies don’t have. I understand that they are “independents” in that they don’t own refining, chemicals or retail, but I still have trouble thinking about an independent E&P company being worth $60+ billion. But just like Exxon buying Pioneer and Chevron buying Diamondback, these “independents” end up being part of the “majors.” Okay, Chevron hasn’t announced their intention of buying Diamondback. Yet. Only a personal opinion. Marshall Adkins and Jeff Bellman from Daniel Energy Partners and I were on a panel at the conference, kicking around ideas of what is going to happen next with supply, demand and the Strait of Hormuz. Finally, I hit Tucson for the Energy Workforce and Technology Council annual meeting, which is the trade association for all of North America’s Oilfield Services Industry. I learned a lot.

Iran. Things could have changed by the time you read this, but I made an exhaustive list of all that is going on in the world today and the way it is trending. I see no reason to list all of the reasons, but it becomes increasingly clear that if the Strait of Hormuz is not opened in the next one to two months, a global recession will be inevitable and a “sub-prime type” crash could occur in the U.S. From private credit to France and the UK failing, Germany staying in recession, the entire third world being forced back in time, and even the strong Asian economies taking a very big hit, as well as global crop yields declining. Oops. I started listing them anyway. How do we get the Strait open? No clue. I just know we have to. Soon.

Highlight. At the TIPRO meeting, one of the most entertaining and informative “presentations” was from the father and son team of Scott and Bryan Sheffield. You understand better the people who make up our industry. I had always made it required reading for those who work for me to read “The Big Rich,” which I think is the best history of our industry, spotlighting the people who shaped the oil industry. This felt like another chapter of the same book. The persistence and confidence, the optimism and lack of cynicism, the intelligence and determination are what have made our industry different from many others, and these two gentlemen gave a very good view that our industry continues to be shaped by the people in it. My bottom line for our three man panel? If we don’t open the Strait soon, a global recession is a certainty.

Moderation in All Things. I was flattered to be asked to moderate a panel at the EWTC meeting this week. The topic was all things offshore. I had a very good group on stage, including Blake Denton, the Senior VP of Marketing & Contracts for Noble, Siva Gollakota, Vice President of Supply Chain for Talos and John Seeger, CEO of Commodore Offshore Operating. The key takeaways?

𝗖𝗮𝗽𝗶𝘁𝗮𝗹 𝗿𝗲𝘁𝘂𝗿𝗻𝗶𝗻𝗴 𝘁𝗼 𝗹𝗼𝗻𝗴-𝗰𝘆𝗰𝗹𝗲 𝗼𝗳𝗳𝘀𝗵𝗼𝗿𝗲 𝗽𝗿𝗼𝗷𝗲𝗰𝘁𝘀. After years of underinvestment, capital is beginning to move back into conventional and offshore resources as shale growth moderates and long-term supply gaps emerge.

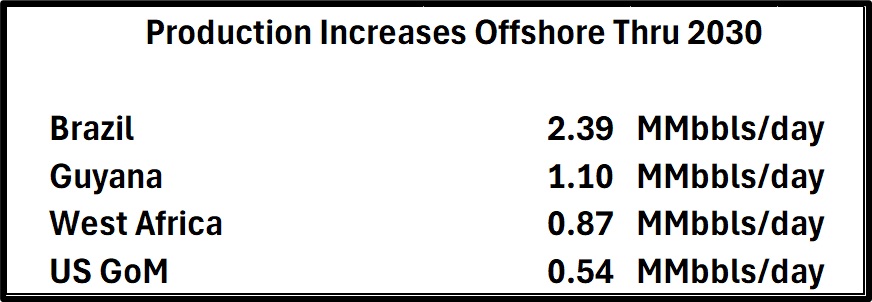

𝗗𝗲𝗲𝗽𝘄𝗮𝘁𝗲𝗿 𝗹𝗲𝗮𝗱𝗶𝗻𝗴, 𝘄𝗶𝘁𝗵 𝗽𝗮𝗿𝘁𝗻𝗲𝗿𝘀𝗵𝗶𝗽𝘀 𝗱𝗿𝗶𝘃𝗶𝗻𝗴 𝗲𝘅𝗲𝗰𝘂𝘁𝗶𝗼𝗻. Deepwater remains the most competitive offshore play, supported by stronger economics and long-term development programs. Strategic partnerships across operators and service providers are critical to improving utilization and delivering consistent results.

𝗧𝗲𝗰𝗵𝗻𝗼𝗹𝗼𝗴𝘆 𝘂𝗻𝗹𝗼𝗰𝗸𝗶𝗻𝗴 𝗲𝗳𝗳𝗶𝗰𝗶𝗲𝗻𝗰𝘆 𝗴𝗮𝗶𝗻𝘀. Advances in automation, machine learning and AI are improving drilling performance, exploration and cost efficiency. The next phase will focus on scaling these capabilities across fleets and operations.

The outlook was clearly positive long-term for offshore, with growing global demand, improving capital access and the need for reliable, large-scale production supplanting any growth in unconventionals in the U.S. and other basins around the world.

Education Continues. The EWTC meeting was especially constructive. With everything that has happened in the last month, and really the volatility of commodity prices, every company has been running all sorts of sensitivity scenarios for their businesses. So instead of a banal discussion on some esoteric topics, all of the sessions involved people looking for answers or indications and trying out explanations of their outlooks on a peer audience.

A session I thought was very germane was the Onshore Operator panel, which focused on the realities of operating across today’s U.S. onshore landscape. It was moderated by Sam Sledge, CEO of ProPetro with a panel of:

Jamie B. Benard, President of SOGC, an advisory firm

Sarah Fenton, Executive VP of Upstream for EQT

Chad McAllaster, Executive VP of Operations for Diamondback

The key points from what was a great discussion:

𝗦𝗮𝗳𝗲𝘁𝘆 𝗮𝘀 𝘁𝗵𝗲 𝗳𝗼𝘂𝗻𝗱𝗮𝘁𝗶𝗼𝗻 𝗼𝗳 𝗽𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲. Safe operations are efficient and cost-effective operations. Strong leadership in the field, proper handoffs and a culture that empowers stop work authority are critical to preventing incidents and maintaining performance.

𝗗𝗮𝘁𝗮-𝗱𝗿𝗶𝘃𝗲𝗻 𝗲𝘅𝗲𝗰𝘂𝘁𝗶𝗼𝗻 𝗮𝗻𝗱 𝗮𝗰𝗰𝗼𝘂𝗻𝘁𝗮𝗯𝗶𝗹𝗶𝘁𝘆. Leading indicators, benchmarking and consistent reporting are driving better outcomes. The more visibility teams have into performance metrics, the more effectively they can manage risk and improve operations.

𝗗𝗶𝘀𝗰𝗶𝗽𝗹𝗶𝗻𝗲𝗱 𝗴𝗿𝗼𝘄𝘁𝗵 𝗶𝗻 𝗮 𝗰𝗼𝗺𝗽𝗹𝗲𝘅 𝗲𝗻𝘃𝗶𝗿𝗼𝗻𝗺𝗲𝗻𝘁. Operators remain focused on funding development through cash flow while managing real-world constraints such as water, power and logistics. The ability to maintain stability while flexing production when needed is a key competitive advantage.

Panelists emphasized that long-term success in onshore operations will come down to consistency, operational discipline and the ability to execute under pressure.

Impairment. We have written in the past few weeks that one risk of the Iran Conflict is that countries are being forced to shut in producing wells, and that shutting in producing wells can negatively impact ultimate recovery from a reservoir. Basic engineering. The longer the well is shut in, the greater the likelihood of some negative impact on future production. Rystad this week put out some numbers out on the topic. They said that about 10,000 wells are currently offline in Kuwait, Iran, Qatar, Iraq, the UAE and Saudi Arabia. In their worst-case scenario of a 6-month shut-in, up to 3,000 of the shut-in wells won’t be able to come back to normal operations without some surface and subsurface work, and another 1,000 would require major workovers. We are back to the basics. The longer this lasts, the more damage is done.

No Fishing Allowed. Oregon has put IP28 on the statewide ballot. It would ban all hunting and fishing in the state in the name of ending animal cruelty. Nor would you be able to raise chickens, cows or pigs for your own consumption. Would IP28 ban hunting in Oregon? IP28 would remove the legal exemption that currently protects hunting from Oregon's animal abuse statutes. All forms of licensed hunting would become criminal acts under Oregon law. It is the PEACE Act (People for Elimination of Animal Cruelty Exemptions). We haven’t heard from PETA in some time. Maybe this is the successor gadfly. A gadfly that you can’t throw with a fly rod to catch that elusive steelhead, only to see the animal cruelty of catch and release.

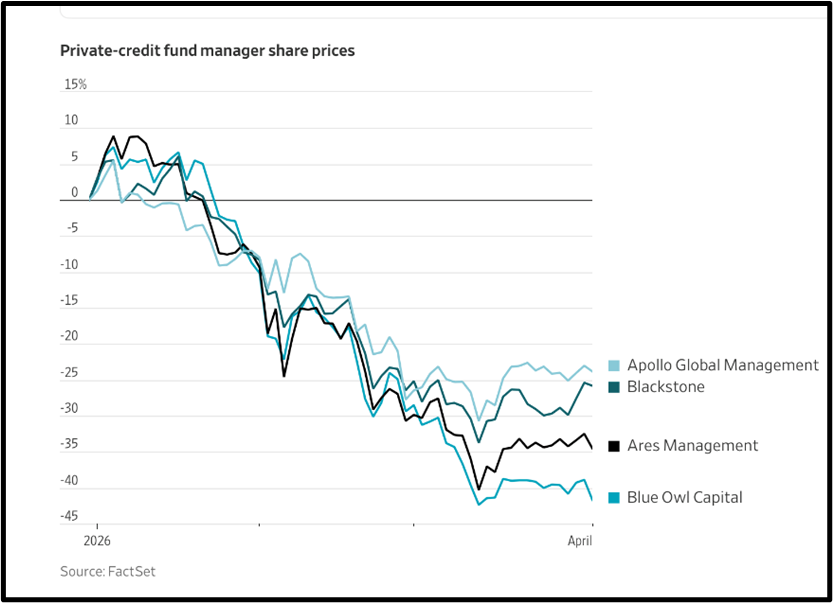

A Big Concern. We have been writing about private debt for some time. The private credit market is now a $1.5 trillion market, the same relative size as the credit markets that sub-prime was when it crashed the market. The market is as big as the syndicated bank loan market. Blue Owl has been the poster child. Amid a scramble to meet redemptions and then restricting them, the stock has dropped by 40%. Rising interest rates, lower bond prices and forced selling due to redemptions magnify the issue into a run on the “bank.” The Treasury Department called a meeting with regulators to discuss risks in the private credit sector amid pushes to include it in 401(k) plans. Investors have requested to withdraw $5.4 billion from two Blue Owl Capital private credit funds. Redemptions are now limited to 5%. The redemptions represented 22% of Blue Owl Capital’s $36 billion private credit fund and 41% of a technology-focused fund.

PPHB U.S. Energy Market Highlights:

Commodity Prices: WTI crude oil is currently $111.54 per barrel (up ~11.9% week-over-week) and natural gas is $2.80 per MMBtu (down ~7.4% week-over-week).

Crude Oil Production: U.S. crude oil production is currently ~13.7 MM BOPD (up ~0.6% year-over-year).

Crude Oil Inventories: U.S. crude oil inventories increased by ~0.5 million barrels week-over-week vs. an estimated increase of ~1.8 million barrels.

Frac Spread Count: There are currently 166 frac spreads operating in the U.S. (increase of 7 spreads week-over-week).

Onshore Drilling Rig Count: There are currently 548 drilling rigs operating in the U.S. (increase of 5 drilling rigs week-over-week).

Doing Better Than Most. While private credit is having a very difficult time, energy credit is doing significantly better. Why? First, we already went through our cleanup period with companies significantly reducing debt from three years ago. After the 2015–2016 and 2020 busts, many E&Ps shifted toward lower leverage, lower capex growth and higher shareholder returns. Reuters reported U.S. rig counts fell about 20% in 2023, 5% in 2024 and 7% in 2025 as firms focused more on paying down debt and returning cash than chasing volume growth. Secondly, capital discipline really matters for creditors. A lender would rather finance a commodity business with a stronger balance sheet, hard assets and management that has stopped over investing at negative returns. Finally, we aren’t distressed right now when many other industries are. Morningstar Dun & Bradstreet said its 2026 North American oil and gas outlook is one of resiliency, even though it flagged as having price volatility and geopolitical risk. Fitch raised its near-term oil and gas price assumptions in March. Higher commodity prices are not universally good for the economy, but for many upstream credits they improve cash flow coverage and near-term refinancing capacity. It might be the tallest midget, but we live in a relative world and we are doing relatively better than most.

Deep Space. As I am sure everyone knows, the Artemis II rocket, with four astronauts on board, launched this week and is the first deep space since Apollo 17 in 1972 over 50 years ago. We do a lot in close sub-orbits. SpaceX has launched over 360 rockets into space in the last 14 years. The company does 80% of all space launches. Artemis II sends astronauts ~250,000 miles from Earth. To put that into perspective, there are three main orbital distances that satellites travel, with the furthest at 23,000 miles. It is a $100 billion effort. There are already plans for the future of the program to achieve even more. Artemis III will allow humans to land on the Moon in 2027 and Artemis IV will help establish the lunar base / space station (Gateway) which will, in the long term, eventually take us to Mars. These projects are already on the drawing board.

This Is The Enemy. It is not the traditional enemy we think of when we think of war and conflict. They are filled with religious fervor and dying for the cause is desirable.

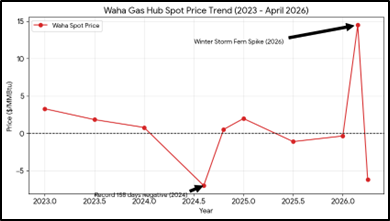

Lemons into Lemonade. The Permian natural gas hub, Waha, traded in negative territory most of 2024 and much of 2025 and is continuing into 2026. Who cares? The Permian produces enough oil at a good price, despite anti-flaring rules being enforced more than in the past. Then we could just burn it rather than paying to have it taken away and selling it at a loss. Regardless of how high oil prices are, paying to get rid of a product that is expected to see 25% growth over the next five years doesn’t seem to make much sense to me. We have long held that this arbitrage between Waha and Henry Hub can’t continue on an academic basis as there is too much stranded gas to practically sell or consume. This is why we have said that west Texas would be a magnet for AI data centers. The players are coming to light. Chevron is an energy pioneer in West Texas, powering some of its operations with its own wind turbines. Engine No. 1 is the activist investor group that took two seats on Exxon’s board in 2021. Finally, there is Microsoft, who needs power for its GPUs. The three have joined forces for an exclusivity agreement for power generation and supply. No commercial terms were revealed. This isn’t new for Chevron and Engine No. 1 since they’ve had a partnership for over a year to develop turbine powered gas-based power plants across the country. They’re using GE Vernon’s turbines. The facility is expected to generate 2.3 GW of power, which is stunning in its own right. That is several million homes. The combination of companies getting together to build, power and manage these AI data centers is getting more interesting by the day. We fully believe that several of the AI data centers currently planned won’t open on time due to constraints on both power and electrical equipment, such as transformers and power supply units. But this is a transformation for Chevron who has evolved from a supplier of molecules to a supplier of electrons, providing end-use power rather than just being a component of the power value chain. “The approach reflects an emerging shift in how power for AI is being developed, bringing energy supply closer to demand through co-located, behind-the-meter generation to deliver reliability while helping avoid added strain on regional electricity systems.” – Chevron.

The Problem with the Numbers. This 2.5 GW installation by Chevron will require 0.3-0.4 Bcf per day of natural gas. The plan is to boost it up to 5 GW. The Permian currently produces 28.6 Bcf per day. There are projections of an incremental 10 Bcf/day of production over the next 5-6 years. That means another 10 data centers could get teed up over the next few years. The one proposed would already the biggest ever, 5 times larger than anything seen before. If you ever wonder if demand for natural gas will go significantly higher, it will. Where it comes from is the real question. While the Permian produces ~28 Bcf per day, the Appalachian basin clocks in at almost 37 Bcf per day and the Haynesville at 15.2 Bcf per day. Those are two other places where data center growth is expected.

Running on Fumes. When the Iran Conflict began, the world was over supplied with oil, with high inventories leading to a weak oil price market. After a month of fighting, surplus stocks have been worked off apart from those barrels trapped in the Gulf. Refineries in Asia are closing from lack of supply. Others are closing due to the heightened price for feedstock. Aviation fuel in many parts of the world is seeing declining inventories, leaving only a few weeks of supply, indicating that airline flights will start getting cut back soon. Jet fuel prices in the U.S. have more than doubled since the conflict began on February 28, 2026, with some regions seeing a year-to-date increase of over 120%. The shortages will be felt most acutely in California, where inventories are seeing very large draws due to reliance on imported product and the closure of a major refinery (Phillips 66 Las Angeles). Any mention of the conflict lasting longer puts more squeeze on oil pricing, increasing volatility and price. Cuba has already seen the cancellation of flights, clear global foreshadowing. Southeast Asia, including Japan, Singapore and South Korea are being impacted, but several countries don’t have the ability to pay up for oil at these prices even if it were readily available. Inventories can often have mixed impacts on oil prices, but the absence of any inventory most definitely has a significant impact. So, now the concern is that the Administration will ban exports to ensure we have enough diesel and jet fuel, two products in short supply that are only depleting at a quicker rate with each passing day. We only import 5% to 10% of our diesel and jet fuel anyway, so while global pricing has gone up, the availability in the U.S. should not be a major issue, even if the economy slows down.

The International Order of Saint Hubertus. Also known as the IOSH, the order is one of the world’s most historic hunting orders. Founded in 1695 by Count Franz Anton von Sporck in Bohemia, the Order was created to honor the legacy of Saint Hubert, patron saint of hunters, to promote ethical hunting, respect for nature and responsible wildlife stewardship. Brought to the U.S. after the Second World War with support from U.S. Ambassador Llewellyn Thompson, General Mark W. Clark and others, the Order has grown into an international community of conservation-minded sportsmen. The Order is currently led by His Imperial and Royal Highness István von Habsburg-Lothringen, Archduke of Austria and Royal Prince of Hungary. Members are individuals of high ethical standing and a deep commitment to conservation. According to tradition, Hubert experienced a profound transformation after encountering a stag bearing a glowing cross between its antlers. Inspired by this vision, he gave up his worldly pursuits and devoted his life to service and piety. The Order’s motto, “Deum Diligite Animalia Diligentes” (“Honour God by Honoring His Creatures”), captures the enduring link between spirituality, nature and responsibility. He died in 727 and was declared a Saint in 743.

Any and all comments, arguments and rebuttals are welcome!

In addition to my association with PPHB, I serve on three private company boards. Merit Advisors is a property valuation company and I have long been a fan of optimizing how a business is run, not just the tools we make. Merit is in the business of savings companies’ money, actual cash, by doing a much more in-depth and realistic view of equipment and reserve valuations and I am very impressed with their work. I am also on the advisory board of Preng & Associates, a leading executive search boutique that specializes in all things related to Energy & Power.

I serve on the Advisory board of the Energy Workforce & Technology Council (formerly PESA), the National Ocean Industries Association (NOIA), and the Maguire Energy Institute at SMU my alma mater.

jim

214-755-3914 | james.wicklund@pphb.com

Leveraging deep industry knowledge and experience, since its formation in 2003, PPHB has advised on more than 180 transactions exceeding $11 Billion in total value. PPHB advises in mergers & acquisitions, both sell-side and buy-side, raises institutional private equity and debt and offers debt and restructuring advisory services. The firm provides clients with proven investment banking partners, committed to the industry, and committed to success.