May 22, 2026

Things I Learned This Week Walking Like an Egyptian

I had a fabulous trip with my kids, celebrating the youngest’s graduation from the University of Colorado, where he earned a business degree in finance and accounting. He was therefore tasked with being our official exchange rate guy and told us how much things cost when looking at the Egyptian pound prices. It was an amazing trip. Cairo was perfectly safe, unless you were in a taxi, or on the road at all. While there are marked lanes, they seem to be more of a suggestion than anything else. Driving there would make me crazy, and I’ve driven in Rome and Paris. Then, as we were leaving Cairo several days later, we realized we had never seen a stoplight in all of Cairo. We saw two in Luxor and none in Aswan. The drivers are fairly polite, but when no one pays attention to the lanes, it still gets stressful. What they do have is bomb-sniffing dogs. Hotels and tourist sites used them every time we came and went.

Hot. I have lived in Texas for years, much of that time in Dallas. The old argument is that Houston is humid, whereas Dallas has a dry heat. I remember saying that back in 1981, when Dallas had a couple of days at 113 degrees. I was a bit younger then, and the heat didn’t bother me too much. Of course, we were making beelines to our cars to crank up the AC or spending a great deal of time indoors complaining about the heat. Being older now, my tolerance has slipped a little, but this week it didn't slip, it fell flat on its face. I spent the last two days in Luxor, Egypt’s ancient capital and home to amazing places like Karnak and the Valley of the Kings. The former sits in the middle of town, while the Valley is in the desert just west of town. Now, you first have to understand that there are no trees. No “not many trees.” None. No bushes, no scrubs nor grass. Nothing. No shade. And it was 114 degrees both days. You live with a water bottle.

Politics. Americans were not hated. We sometimes claimed to be Canadians since no one hates Canadians, but most everyone was friendly and helpful. There was little comment about Iran. The Suez Canal, a major economic engine for the country, was shut down for eight years following a war with Isreal, so the idea of the Strait being closed for several weeks didn’t evoke much feeling. Egypt gets much of its power from the Aswan Dam and buys natural gas from Isreal’s Leviathan gas field project. Oil production in the western desert also contributes to the mix. There is little love lost between Iran and Egypt, and it is not much of a distraction in the latter.

U.S. Oil and Gas. There hasn’t been much to talk about. Until the Strait opens, the global economy is in trouble. It is very binary. When the Strait reopens, crude oil prices will fall, but not by much. We aren’t going back to the $65 per barrel levels from before the Iran conflict. Our math shows that $75-$78 oil price is a reasonable target, but I know better than to predict actual prices. A risk premium that didn’t exist before now does. That reality, along with the lifting of the back end of the curve, means that U.S. activity will likely be higher than we had previously expected. But before the party starts, remember that U.S. spending was already expected to decline. Better than expected is still better, but it doesn’t automatically imply nirvana. The place, not the band! Pressure pumping companies are raising prices, as are rigs operators and other equipment providers. Any positive bias to margins and returns is a good thing, but much of the near-term activity will likely be focused on infrastructure repair rather than traditional oilfield services support. Still, it is all headed in the right direction. It just comes down to one thing. When does the Strait open? We have lost ~1.2 billion barrels of oil production, with losses still climbing, alongside drained inventories and record exports. Things will remain tight, and may tighten further. But until the Strait opens, no one’s crystal ball has much to say.

Top Story This Week. Energy this week, particularly LNG, appears to once again be front and center in the global hydrocarbon discussion. The decision to export LNG was made under the Barack Obama administration. Instead of assigning the feasibility study to the Commerce Department, the administration reportedly gave it to the national security apparatus, which approved the exports in only a few weeks, arguing that the ability to trade large cargoes of energy with strategic partners was invaluable. When the Russia-Ukraine War broke out, U.S. LNG came to the rescue of Europe and continues to do so. Asia has also been a major beneficiary of the U.S. LNG business, with the expansion of the Panama Canal allowing much shorter transit times from LNG facilities along the U.S. Gulf Coast to that part of the world. Volumes continue to increase. The fact that Qatar has experienced damage to two of its LNG trains means it will not immediately be able to fulfill all of its contractual obligations, even if the Strait were to reopen. Once again, U.S. LNG is picking up the slack. Energy security remains one of the hottest topics globally. It is something the U.S. doesn’t have to dwell on quite as much given how energy independent it has become, but other parts of the world are only beginning to address the issue. LNG is clearly riding to the global rescue. China is trying to improve its own energy security by accelerating the development of shale gas across parts of the country. Meanwhile, BP is reportedly restructuring parts of its gas trading business to focus more heavily on LNG.

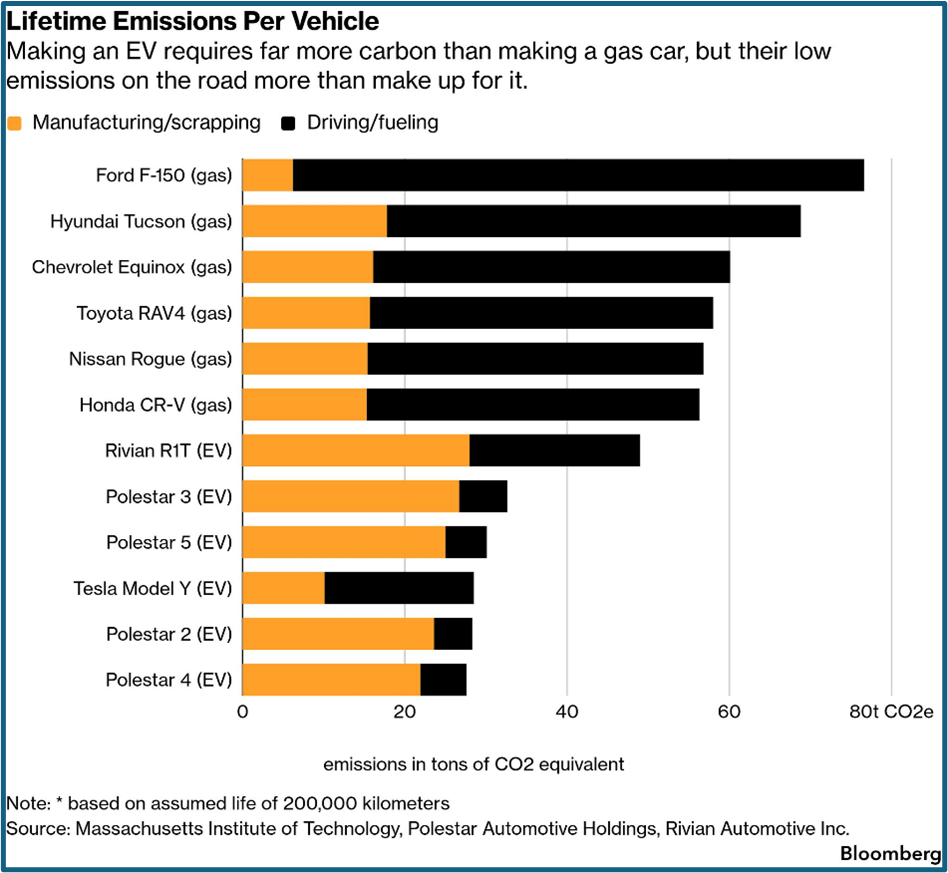

Hold On. Many have celebrated the changes in outlook by the major automotive companies regarding the future of electric vehicles. Detroit has famously taken over $20 billion in charges and write-downs associated with its EV future. We have long said that hybrids make the most economic sense and that many electric vehicles are fun to drive but don’t pass the full-cycle economics test, even when talking about sustainability. But nobody ever said they were going away, and they’re not. In the U.S., we have limited availability of low-cost electric vehicles. The average cost of a gasoline-powered vehicle is about $47,000, while the average cost of an electric vehicle is around $60,000. But with advancements in markets and technology, that is beginning to change. China has a whole line of $30,000 electric vehicles with good range, advanced technology and attractive designs. But they aren’t allowed in the U.S. yet. To be fair, Detroit is working to roll out some EVs in the $30,000 range, but it remains well behind the curve. There are also hefty tariffs on Chinese EVs in the European Union. The rest of the world has liked what it has seen and is liking it more every day. A major driver of that trend is the current oil crisis.

Balance in All Things. Whether you have to pay California gasoline prices or not, no one can deny the fact that oil prices, and therefore gasoline prices, are up. We are in the middle of a global energy crisis. That is what the headlines say, and the prices seem to agree. What to do? Don’t buy a gasoline-powered car when your primary operating cost is subject to the politics of a religious authoritarian state. More people are concluding that the electrical grid is a more reliable, and likely cheaper, alternative. As a result, EV sales were up 20% last year and represented one-quarter of all car sales globally. The EU experienced the strongest EV growth, with sales increasing by more than 30%, driven mainly by the stricter EU CO2 standards for cars. EV sales in China were ~55% of total vehicle sales, compared to only ~10% in the U.S. From a global perspective, that gap likely normalizes over time. But the likelihood of a steep decline from China’s ~55% penetration rate strikes me as low, which means the U.S. figure has to grow significantly.

The Players. China automakers supplied 60% of global electric car sales in 2025, while European and North American automakers were each responsible for about 15% of global sales. This information comes from the Global EV Outlook, an annual publication that identifies and assesses recent developments in electric mobility across the globe and serves as the flagship EV publication of the International Energy Agency.

PPHB U.S. Energy Market Highlights:

Commodity Prices: WTI crude oil is currently $101.16 per barrel (down ~4.6% week-over-week) and natural gas is $2.91 per MMBtu (up ~0.7% week-over-week).

Crude Oil Production: U.S. crude oil production is currently ~13.7 MM BOPD (up ~2.3% year-over-year).

Crude Oil Inventories: U.S. crude oil inventories decreased by ~7.9 million barrels week-over-week vs. an estimated decrease of ~7.9 million barrels.

Frac Spread Count: There are currently 184 frac spreads operating in the U.S. (increase of 5 spreads week-over-week).

Onshore Drilling Rig Count: There are currently 558 drilling rigs operating in the U.S. (increase of 7 drilling rig week-over-week).

And Why? No one trusts oil prices anymore and the ability of the OPEC and OPEC+ cartels are diminished by the departure of a core member. The Strait of Hormuz remains closed, and, even when reopened, there will be a risk premium associated with oil that has to transit through the Strait, regardless of any agreement or economics. Buy a high-end Tesla for $80,000, knowing that rental car agencies have been shedding Tesla because of the lower-than expected resale value and high repair cost. There just aren’t that many wealthy people who have that much money for a car, especially one with so many potential issues. But for $30,000? Not to mention it’s fast, looks cool, has a giant screen and all the bells and whistles? A very different economic decision and with a much more crowded demography. Save the planet? Heck no. Just trying to save some money without losing face.

Very Well Said! “We are future-proofing our company for the inevitable climate-neutral society that will come,” said Head of Sustainability Fredrika Klarén. “We’re not doing this just to be good; we’re doing it to be smart.”

Spinning Power. We all know the mantra – turbines are 2-3 year back-ordered, so, if you are looking to meet your power needs, what does the market look like? Siemens is one of the big three turbine manufacturers used for electric power generation. One of their executives recently gave an interview that gave a very interesting picture of the current market:

Companies are getting orders that are double the size of what their entire factory can produce in a year.

No sales pitch or analysis on air quality or emissions is needed, they just want to place the order.

Some backlogs are running 5-6 years with transformers and inverters even longer.

“Sustainability” is out, reliable power, at any price, is all that is wanted.

Orders have gone from previous 20-30 MW orders to now 200-500 MW units.

Some double booking is going on for transformers and switchgears because of the extra-long lead times.

Margins have gone from 4-6% a couple of years ago, to 20-23%, and, in some cases, even 40%.

Data center builders are great customers, caring more about availability than price.

AI is not just about the chips used. It is a huge industrial buildout story. And whether you like AI, don’t like AI or you don’t think the chip companies will earn its valuation, fine. But the companies that supply the material, products and labor or construction for the buildout? Picks and shovels. Many of us have very mixed feelings about AI and its future. From a business perspective, there are truisms about the technology whether it is approved of our not.

AI is becoming a massive industrial buildout story, not just a technology story.

Electricity availability is increasingly the pivotal factor for AI growth.

Natural gas, turbines, transformers, and grid infrastructure is now becoming “critical AI infrastructure.”

The market is moving from “lowest-cost power” to “fastest-available reliable power.”

Supply chain bottlenecks in electrical equipment may become as important as semiconductor shortages were during the last tech cycle.

As An Aside. “In El Paso, Texas, Meta is powering a $10 billion AI campus with 813 hospital backup generators because the gas turbines they actually need won’t arrive for another decade. Meanwhile, in Louisiana, they are building another 7GW of gas plants to feed the next datacenter.”

And Again. The company currently runs 46 natural gas turbines at its data center, mounted on flatbed trailers because the state classifies it as mobile equipment and exempt from air pollution regulations for one year. The company has permits for only 15 of the turbines currently operating at the facility.

And So It Goes. Pakistan gets rewarded for U.S.-Iran mediation with LNG! Diplomacy pays in cargoes.

Diversity. “Remote lithium operations often lack reliable formation data due to logistics and limited logging access. Compact™ shuttle logging technology delivers wireline-quality data in a portable format for remote sites, improving reservoir insight and decisions.” – Weatherford advertising its mining business.

Open the Crypto Gates! President Trump signed an executive order to reduce regulatory barriers and voiced support for the integration of digital assets, crypto currencies and other aspects of our daily financial life. Blockchain is reemerging as a focus. Federal regulators will review all the processes and rules that might limit “innovation.” The Federal Reserve will be asked to evaluate whether non-bank financial companies, including digital asset firms, can directly access the Reserve window as well as payment accounts and services. This is the new effort to streamline processes and to limit issues involving volatility and risk. Regulators have 90 days to identify barriers, while the Federal Reserve has 120 days to deliver its findings and recommendations to the White House.

Deterrent. So, the U.S. has struck a deal to send captured illegal immigrants overseas. The UK did the same thing last year, sending arrested migrants to Rwanda. To some, that sounded cruel. The U.S. is sending them now to the Congo. If that isn’t a deterrent, I’m not sure what is. I would self deport to Mexico. Now.

Before you get into an argument, remember this quote: “A bee does not waste its energy trying to convince a fly that honey is better than shit.”

Headlines.

YPF unveils $25-billion investment plan to accelerate Vaca Muerta exports.

Solaris Energy Infrastructure Announces Completion of $2 Billion financing and expansion of existing power contract.

Atlas Shares a recovery roadmap: Strong pricing with no “V” shapes in its forecast for the foreseeable future.

NATO weighs Hormuz mission as shipping disruptions escalate.

U.S. sanctions 19 vessels through expanded crackdown on Iranian oil exports.

The dividend yield on the S&P 500 is on the verge of an all-time low and artificial intelligence is to blame.

It Finally Shows Up. In 2023, California passed two big climate disclosure laws. Now, implementation of those laws will bring about more environmental reports for major companies. Starting August 10th of this year, many companies will have to begin reporting their direct greenhouse gas emissions. If you are doing more than $1 billion in global revenue and do any business in California, you are subject to the new reporting requirements. Scope I and II reporting begins this year. Next year, Scope III is required. It is Scope III that is the problem, because it includes emissions from suppliers, transportation, product use, contractors and sometimes customers. For our industry, that is anyone that drives an internal combustion engine car. The issue is that even companies that are below the revenue threshold will still have to supply all that information to the large customers who must provide the report. Think of every company or individual who does any work with Exxon or Chevron. Who wins? Carbon accounting firms, auditors, law firms, data management providers and verification companies.

Hobo with Garbage Can Stuck on His Head Mistaken for Met Gala Attendee

The Problem. Many firms are discovering they currently cannot measure emissions accurately across global supply chains. It is expected to cost large companies millions to set it all up, and millions more to keep up. While Sarbanes Oxley showed that corporate America could comply with detailed disclosures, this will cost huge sums of money and are likely not to accomplish much. Keep in mind that the largest companies will have to get detailed information on how every product they sell impacts emissions, and they will have to get that data from their suppliers, contractors, vendors, logistics providers, drilling contractors, equipment makers and customers. As an example, an E&P company’s Scope I emissions comes from drilling rigs, compressors, flaring and other wellsite processes. But Scope III can include the downstream combustion of all produced hydrocarbons. It could be one of the more impactful accounting changes of the decade.

Any and all comments, arguments and rebuttals are welcome!

In addition to my association with PPHB, I serve on three private company boards. Merit Advisors is a property valuation company and I have long been a fan of optimizing how a business is run, not just the tools we make. Merit is in the business of savings companies’ money, actual cash, by doing a much more in-depth and realistic view of equipment and reserve valuations and I am very impressed with their work. I am also on the advisory board of Preng & Associates, a leading executive search boutique that specializes in all things related to Energy & Power.

I serve on the Advisory board of the Energy Workforce & Technology Council (formerly PESA), the National Ocean Industries Association (NOIA), and the Maguire Energy Institute at SMU my alma mater.

jim

214-755-3914 | james.wicklund@pphb.com

Leveraging deep industry knowledge and experience, since its formation in 2003, PPHB has advised on more than 180 transactions exceeding $11 Billion in total value. PPHB advises in mergers & acquisitions, both sell-side and buy-side, raises institutional private equity and debt and offers debt and restructuring advisory services. The firm provides clients with proven investment banking partners, committed to the industry, and committed to success.